Lexicon Financial Group Weekly Update — March 18, 2026

“Nothing connected to the internet is truly safe, but security by design can reduce risk significantly.”

From the desk of Craig Swistun, CIM, MFA-P, Portfolio Manager, Raymond James Investment Counsel, and Wayne Hendry, Client Relationship Manager, Raymond James Investment Counsel

ISSUE 220

Looking Around

Although we continue to monitor the ongoing Iran war and its impacts, it is not the focus of your weekly update this week. Instead, the focus is on artificial intelligence (AI) and the cybersecurity sector. Please click on the link below to read all about this.

Artificial Intelligence and Cybersecurity

Looking Back

Stock markets in Canada and the United States (U.S.) lost ground last Friday, as the Iran war continued to hike oil prices higher and increase investor anxiety about what an ongoing closing of the Strait of Hormuz means for inflation and interest rate policy.

Read and Watch

Want deeper insight into topics in your Weekly Update? Then, read and/or right click:

Canada sheds more than 100,000 jobs in first two months of year

Video: The US economy may be strong — but it's delicate

Middle East war having 'huge impact' on EU economy: Commissioner Christophe Hansen

Revised data shows Japan economy grew on strong investment

China’s economic outlook: trends, challenges and opportunities

The S&P/TSX composite index (TSX) finished last week down 1.6 per cent. According to Brian Madden, chief investment officer with First Avenue Investment Counsel, this pullback appears to be a defensive rotation within the TSX, with lower-risk areas of the market, like consumer non-cyclicals, utilities and real estate, seeing gains. These gains were offset by losses in the basic materials sector as the price of gold moved lower. Canadian investors also sifted through a fresh report from Statistics Canada showing the economy faced ugly job losses in February, which suggested that the labour market is struggling after nearly a year of U.S. tariff pressures. (1)

Unsurprisingly, major U.S. stock markets declined for the third straight week due to the ongoing Iran war and the resulting volatility in oil markets dominated headlines. Oil prices were volatile throughout the week, as investors weighed the risk of prolonged supply disruptions through the Strait of Hormuz, a major shipping route for oil, against intermittent signs of potential de-escalation.

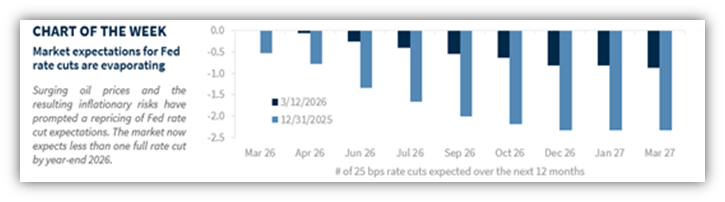

Investor sentiment was not helped by the Bureau of Labor Statistics report that nonfarm payrolls declined by 92,000 in February – much less than the expected gain of around 60,000 – and that the unemployment rate ticked up to 4.4 per cent. This could complicate interest rate decision-making by the U.S. Federal Reserve (Fed), as policymakers try to balance signs of labour market cooling against potential inflation pressures from rising energy prices.

Source: Raymond James

Other sources of uncertainty—including heightened concerns around stress in private credit markets and ongoing developments in trade policy—also appeared to weigh on investor sentiment during last week. Meanwhile, the Bureau of Economic Analysis (BEA) reported that the Fed’s preferred inflation gauge, the core personal consumption expenditures (PCE) price index, increased 0.4 per cent in January, roughly in line with expectations, while the annual rate unexpectedly ticked up to 3.1 per cent – the highest level since early 2024.

The BEA also reported that the U.S. economy grew at a slower pace than initially estimated in the fourth quarter of 2025. The second estimate for gross domestic product (GDP) growth came in at an annual rate of 0.7 per cent versus the initial estimate of 1.4 per cent. This downward revision was due to lower exports, consumer spending, government spending, and investment. U.S. Treasuries generated negative returns last week as geopolitical risk, particularly uncertainty over the Middle East conflict's duration and energy market impacts, and some firm inflation data helped push yields higher. (Bond prices and yields move in opposite directions.)

Amidst heightened uncertainty and volatility, the pan-European STOXX Europe 600 Index declined last the week by 0.47 per cent in local currency terms. The focus of investors appeared to be on how long the conflict in the Middle East is likely to last, what trajectory energy prices will take, and the possible impact on economic growth across the region. Other major European stock markets all ended down last week.

Japan’s stock markets fell last week, as investors watched energy markets closely as Iran-related disruptions around the Strait of Hormuz increased risks to oil supply and heightened volatility in crude prices. Japan is heavily reliant on Middle Eastern oil imports and so, is vulnerable to supply shocks that could push up energy costs and inflation.

The Japanese Yen hovered around its lowest levels since July 2024, when authorities last conducted a major currency intervention to counter the yen’s sharp depreciation. There is some speculation that they could step in again in the future. There was good news, as Japan’s GDP expanded in the fourth quarter of 2025 by more than initially reported, with the economy growing at an annualized pace of 1.3 per cent versus the prior quarter and faster than the preliminary estimate of 0.2 per cent. This upward revision was driven by higher business investment and consumer spending.

Chinese equity markets were mixed over last week. Consumer inflation accelerated to its fastest pace in more than three years, as Lunar New Year holiday spending boosted demand for travel and tourism services. The consumer price index rose 1.3 per cent in February from a year earlier. Core inflation, which excludes volatile food and fuel prices, increased 1.8 per cent year over year, which is the highest since March 2019. Meanwhile, producer prices remained in deflation for the 41st consecutive month, even though the pace of decline eased to its mildest since July 2024, supported by higher metals and oil prices. (2)

The opinions expressed are those of Craig Swistun and not necessarily those of Raymond James Investment Counsel which is a subsidiary of Raymond James Ltd. Statistics and factual data and other information presented are from sources believed to be reliable, but their accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James advisors are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters.

Stock markets fall as oil prices continue to rise amid the release of economic data, The Canadian Press via BNN Bloomberg, March 13, 2026

Global markets weekly update - Oil prices volatile amid Middle East conflict, T. Rowe Price, March 13, 2026

SUBSCRIBE

If you’d like to automatically receive the Weekly Market Update by email, enter your email address in the box below.

We respect your privacy, and you can always remove yourself from the mailing at any time.

Looking to Learn?

If you want to know more about some of the topics we wrote about this week, just click on the links below:

AI is the greatest threat—and defense—in cybersecurity today.