Lexicon Financial Group Weekly Update — June 24, 2026

“The bill always comes.”

From the desk of Craig Swistun, CIM, MFA-P, Portfolio Manager, Raymond James Investment Counsel, and Wayne Hendry, Client Relationship Manager, Raymond James Investment Counsel

ISSUE 234

Looking Around

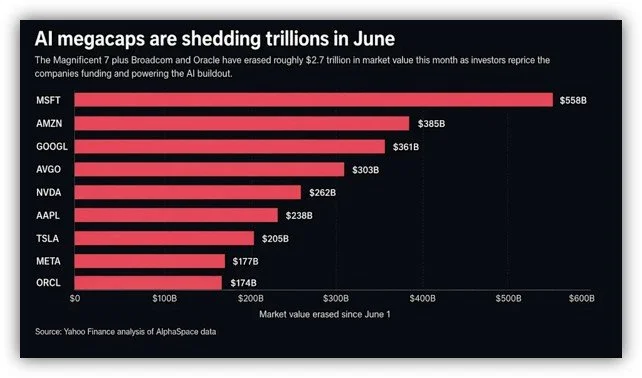

Is the artificial intelligence (AI) bill coming due?

Maybe. The "Magnificent Seven" stocks (Apple, Alphabet, Amazon, Meta, Nvidia, Microsoft, and Tesla) plus Broadcom and Oracle have lost roughly US$2.7 trillion in market value in June, according to Yahoo Finance analysis.

Nvidia and Broadcom are tied to the AI hardware boom. Microsoft, Alphabet, Amazon, Meta and Oracle are tied to the AI spending boom. Apple and Tesla remain part of the megacap growth trade that investors have treated as AI-adjacent. For the last few years, these companies have been drivers of the global economy, but the market appears to be putting a price on the AI build-out.

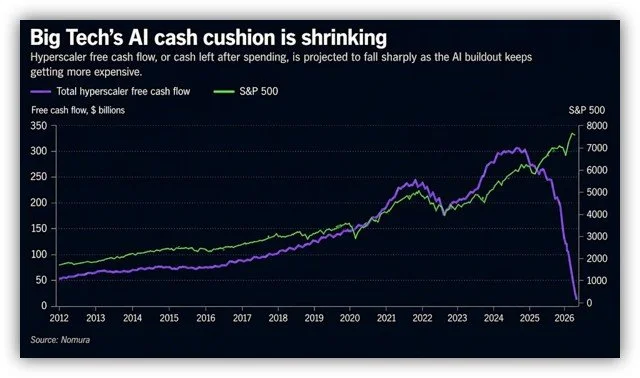

And, as the AI build-out continues, any cash cushion investors have come to expect from the biggest technology platforms is getting squeezed. Data centres, chips, power, networking gear, and cloud infrastructure are becoming the expensive entry fee for staying in the AI race.

Consequently, it is beginning to look like the biggest AI companies are no longer trading solely on the promise of future revenue. Rather, they are trading on the cost of getting there. (1)

However, according to some analysts, the party in the U.S. stock markets is not yet over. The decline in these markets is being seen as "healthy" and a necessary "gut check" after a scorching rally that drove benchmark indexes to a series of records. According to Morgan Stanley Investment Management senior portfolio manager Andrew Slimmon, this week's sharp sell-off, which took down high-flying chip stocks and hyperscalers alike, was to be expected. Slimmon contends that changing expectations around the Federal Reserve's (Fed) monetary policy, from definitely cutting to possibly raising interest rates, helped cause this rout. Higher rates are usually considered a headwind for growth stocks because they increase borrowing costs for companies investing heavily to create future lines of business. Another possible contributing factor here is that investors are taking profits, which is leading to a "moment of pause" in the markets. (2)

Diversified investors have certainly benefited from the rise of technology stocks. As the importance of these stocks in the economy has grown, so has client exposure to these sectors. It’s a cautionary tale, though. Because if one measurement of risk is not having assets available when you need it, going “all in” on a single sector or stock opens investors up to the possibility of needing money at the precise time there is a correction.

Things change quickly. That’s why it’s always prudent to review your short-, medium-, and long-term goals and objectives. Because the more we understand what you are trying to accomplish with your investments – fund daily expenses in retirement, save for a new home, set aside assets for charitable giving, manage tax more efficiently – the better equipped we are to align your investment strategy. If you’re thinking about this, don’t hesitate, let’s book a meeting and go over it together.

Read and Watch

Want deeper insight into topics in your Weekly Update? Then, read and/or right click:

TSX edges lower for week as gold miners slump

Federal Reserve holds rates steady but signals possible hike before year’s end

Nikkei Index Soars Over 70,000 for First Time

Unboxing China: How Dragon Boat Festival illuminates China's night economy

Looking Back

Canada's S&P/TSX composite index fell last Friday to post a slight weekly decline, as a drop in the price of gold weighed on metal mining shares. For the week, the TSX was down 0.2 per cent but it was still up 9.92 per cent for the year. (3)

Most major U.S. markets closed higher last week (which was shortened due to the Juneteenth holiday last Friday), with sentiment broadly supported by news that the U.S. and Iran had signed a memorandum of understanding which cleared the path toward reopening the Strait of Hormuz and helped push oil prices lower.

The Nasdaq Composite fared best by advancing 2.43 per cent while the Russell 2000 and S&P 500 Indexes ended up 1.21 per cent and 0.93 per cent, respectively. Risk appetite improved late last week, however, following reports of progress toward a U.S.-Iran agreement and President Donald Trump’s cancellation of planned strikes. Also, the highly anticipated IPO of rocket and satellite company SpaceX was also a major focus during the week, with the company completing the largest IPO on record on Friday.

The Fed left the federal funds rate target range unchanged at 3.50 per cent to 3.75 per cent last Wednesday. Although this was widely expected, the Fed’s updated Summary of Economic Projections and Fed Chair Kevin Warsh’s first post-meeting press conference were largely interpreted as leaning hawkish in terms of interest rates. Nine of 18 officials penciled in at least one rate hike in 2026, while only one projected a cut. This triggered a sell-off in stocks and a rise in short-term Treasury yields on Wednesday afternoon. U.S. Treasuries generated negative returns through much of last week, with short-term yields rising sharply following Wednesday’s Fed meeting and the yield on the two-year U.S. Treasury note hitting its highest level in more than a year. (4)

European shares inched lower on Friday, as mining stocks tracked a fall in metals prices and investors remained cautious after U.S.-Iran negotiations to end the Middle East conflict stalled. The pan-European STOXX 600 index closed 0.2 per cent lower, still managing to eke out a 0.4 per cent weekly gain after hitting record highs earlier last week. Risk sentiment remained shaky, as U.S.-Iran talks in Switzerland planned for Friday were cancelled as fighting flared in Lebanon, which generated more uncertainty. An uptick in oil prices on Friday sent travel and leisure stocks down 0.9 per cent while energy stocks climbed 1.3 per cent. Mining stocks led losses as commodities prices eased, declining 2.1 per cent. Equities in Europe have been under pressure since the war began due to the inflationary impact of surging oil prices, and sentiment is yet to recover fully due to the frailty of the peace negotiations. (5)

Japanese markets closed up last week as investors reacted to data showing Japan’s core inflation held steady at 1.4 per cent in May. This was in line with expectations, which suggested that underlying price pressures remain under control despite higher energy costs. Market sentiment improved after the U.S.-Iran peace agreement helped push oil prices lower, which eased concerns about inflation. Japanese equities also benefited from a global rally in semiconductor and artificial intelligence-related stocks, which helped offset pressure from the U.S. Fed’s hawkish stance. Sector-wise, technology stocks were mostly higher, while financial, industrial, and consumer shares generally underperformed. (6)

Chinese markets closed mixed last Thursday, with technology stocks leading gains after regulators pledged stronger support for innovation at the Lujiazui Forum. Investor sentiment in the technology sector improved after the Chinese government announced measures to direct more funding toward emerging technologies amid growing competition with the U.S. Authorities said they would support stock market listings for startups in future industries such as quantum technology, nuclear fusion, and brain-computer interfaces. Chinese markets were closed on June 19 for the Dragon Boat Festival holiday. (7)

The opinions expressed are those of Craig Swistun and not necessarily those of Raymond James Investment Counsel which is a subsidiary of Raymond James Ltd. Statistics and factual data and other information presented are from sources believed to be reliable, but their accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James advisors are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters.

Big Tech's $2.7 trillion AI bill comes due: Chart of the Day, Jared Blikre, Yahoo! Finance, June 24, 2026

Why The Market's 'Moment of Pause' Might Be The Breather Tech Stocks Needed, Crystal Kim, Investopedia, June 23, 2026

TSX posts slight weekly decline as gold mining shares fall, Fergal Smith, Reuters, June 19, 2026

Global markets weekly update - Fed holds rates steady; BoJ raises to 31-year high, T. Rowe Price, June 18, 2026

European stocks tick lower as mining losses weigh, Sruthi Shankar and Shashwat Chauhan, Reuters via Yahoo Finance, June 19, 2026

Japan stocks end mixed as inflation remains stable and global tech rally supports sentiment, Business Standard, June 19, 2026

China markets end mixed as technology stocks gain on policy support, Business Standard, June 18, 2026

SUBSCRIBE

If you’d like to automatically receive the Weekly Market Update by email, enter your email address in the box below.

We respect your privacy, and you can always remove yourself from the mailing at any time.

Looking to Learn?

If you want to know more about some of the topics we wrote about this week, just click on the links below:

Hyperscalers: What They Are and How They Work

Tech Stocks Face a Valuation Reckoning as Rate Expectations Harden