Lexicon Financial Group Weekly Update — July 1, 2026

“I think I’m pretty good at long run expectations, but I don’t think I’m good at short-term wobbles. I don’t have the faintest idea what’s going to happen short term.”

From the desk of Craig Swistun, CIM, MFA-P, Portfolio Manager, Raymond James Investment Counsel, and Wayne Hendry, Client Relationship Manager, Raymond James Investment Counsel

ISSUE 235

Looking Around

Geoffrey Chaucer, in his 14th-century work, The Canterbury Tales, noted that “time and tide wait for no man.” Blink, and we’re already halfway through 2026.

Around this time, many financial institutions publish a stock market outlook for the second half of the year. We’ll read them as we always do, but we don’t take them as gospel truth. Because nobody can truly predict the direction of the markets, we remember to stay diversified across multiple asset classes and sectors.

Let’s look at a few of these outlooks.

Conflict in Iran may have dominated the news cycle, pushing out other important first-half-of-the-year stories. It wasn’t that long ago that the increasing investment in artificial intelligence (AI) was all anybody could talk about. Now? How can economies continue to deal with potentially higher energy prices? T.Rowe Price sees a potential danger here – although risk assets (stocks, commodities, etc.) have remained relatively strong amid this instability, the danger is in mistaking this resilience for calm. Thanks to the on-again and off-again Middle East conflict, policymakers globally are prioritizing energy security, domestic production, and supply chain leverage over efficiency and integration. This will most likely widen regional divergences, as globally exposed and trade-sensitive sectors face pressure. Stock markets have remained relatively strong this year but continued economic fragmentation is likely to drive a more differentiated and volatile environment.

On top of this, the fight against rising inflation is looking increasingly challenging. Central banks appear to be abandoning or reversing rate-cutting cycles due to the energy shock, and the possibility of stagflation is further complicating monetary policy in some countries. At the same time, a global manufacturing recovery and rising industrial prices are adding to inflation pressures. Markets appear to be underestimating the longer-term inflation risks for now. (1)

It’s worth remembering that interest rates and inflation generally move in opposite directions. When rates are low (or lowered), the cost of borrowing goes down. More borrowing equates to more spending in the economy, which drives up prices. It’s about finding an equilibrium.

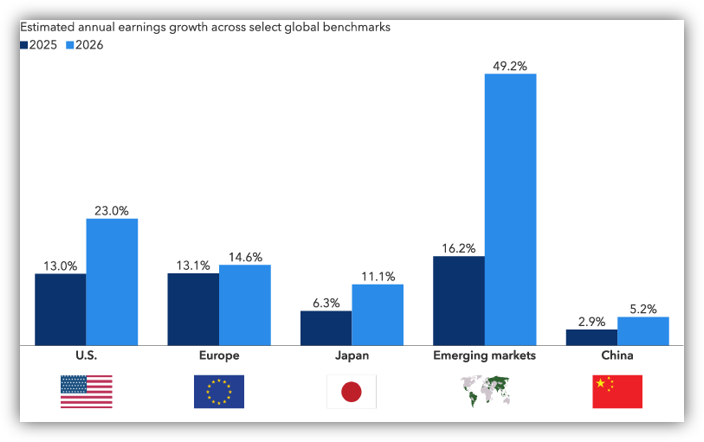

Capital Group questions how, so far in 2026, stock markets have reached a series of new highs amid wars in the Middle East and Ukraine, fluctuating oil prices and elevated inflation. The answer comes down to a simple yet critical factor: corporate earnings have been strong, and markets are rewarding companies with strong earnings under the belief that they can be repeated in the future.

Aggressive spending by technology companies has translated into revenue and earnings growth for companies across other sectors too. Banks are capitalizing on higher interest rates, innovative therapies are driving sales growth in healthcare, and higher crude oil prices are pumping up energy companies. Looking forward, consensus earnings estimates reflect continued strength, particularly in emerging markets by year’s end.

Robust earnings growth is not just a U.S. phenomenon

Sources: Capital Group, FactSet, MSCI, S&P Global.

Global AI spending is showing no signs of slowing. And total global investment in AI infrastructure and AI-related products could reach US$30 trillion over the next decade. All this spending has translated into soaring demand for advanced semiconductor makers like NVIDIA and Broadcom as well as semiconductor foundries like Taiwan Semiconductor Manufacturing Company (TSMC) and networking companies like Cisco Systems, for example. Also, AI cannot run without the physical economy. Demand for steel, copper, heavy construction services and power generation equipment is soaring in support of the AI data centre build-out. All of that said, the surging energy prices, elevated inflation and the market volatility immediately after the start of the Iran War in late February are reminders that maintaining well-diversified, balanced portfolios is crucial in any market environment. (2)

According to J.P. Morgan, following relatively sluggish growth in late 2025 and early 2026, the United States (U.S.) economy is entering the second half of 2026 with increased momentum. Consumer spending is being bolstered by the spending of upper-income households who have seen huge gains in wealth over the past four years. J.P. Morgan expects real GDP growth to continue to accelerate but then slow down in late 2026. They also believe the U.S. Federal Reserve (Fed) will hold interest rates steady for the rest of this year. For many, the right investment strategy, going forward, is to focus on portfolio basics such as appreciating the fundamentals, balancing expectations and diversification. (3)

Read and Watch

Want deeper insight into topics in your Weekly Update? Then, read and/or right click:

Canadian economy grows 0.5% in April after technical recession

AI hopes and fears dominate global central bank meet

European shares slip on global tech slump; Zalando down on regulator action

Japan markets tumble as tech stocks come under pressure

‘We’re not that wealthy’: Beijing’s answer to China Shock 2.0

Looking Back

The S&P/TSX Composite Index (TSX) ended up slightly (0.4 per cent) last week, as higher gold prices boosted metal mining shares but the gains for the TSX were kept in check as investors worried about the inflationary impact of the AI boom. The TSX is headed for a possible 6.8 per cent gain in the second quarter, which would be its eighth straight quarterly advance. (4)

Major U.S. stock markets ended last week mixed. Renewed weakness in large-cap technology and artificial intelligence (AI)-related shares weighed heavily on the Nasdaq Composite and S&P 500 Index while the small-cap Russell 2000 Index and Dow Jones Industrial Average advanced 1.01 per cent and 0.60 per cent, respectively. The Bureau of Economic Analysis (BEA) also reported that its personal consumption expenditures (PCE) price index rose 0.4 per cent in May, matching April’s increase, while the core PCE price index—which excludes food and energy costs—rose 0.3 per cent, unchanged from the prior month. On a year-over-year basis, headline PCE inflation accelerated to 4.1 per cent, the highest since April 2023, while core PCE inflation edged higher to 3.4 per cent, the highest since October 2023. Despite this, personal income and personal consumption expenditures both increased 0.7 per cent in May. Both of these were ahead of consensus estimates, pointing to continued consumer resilience. The increase in spending was also relatively broad-based and led by gains in financial services and insurance, health care, housing and utilities, and energy goods. U.S. Treasuries advanced last week, with yields moving lower across most maturities as oil prices declined and the May PCE data came in roughly in line with expectations.

In Europe, pan-European STOXX Europe 600 Index ended the week up 0.04 per cent in local currency terms. After a positive start to the week, global technology stocks sold off on Friday amid concerns over elevated valuations in AI-related stocks. Major stock indexes in Europe ended down for the week.

Japan's stock markets declined last week as a global technology sell-off later in the week prompted profit-taking in the sector. For Japan, a major importer of Middle Eastern oil, declining oil prices were favourable for as they eased concerns about energy import costs and inflationary pressures. Brent crude, the global benchmark, fell back to pre-Iran war levels, helping support demand for Japanese government bonds (JGBs). The yield on the 10-year JGB declined to 2.60 per cent from 2.64 per cent at the end of the previous week.

Stock markets in China ended last week lower as an early rally in AI and semiconductor-related shares gave way to a broader regional technology sell-off late in the week. (5)

The opinions expressed are those of Craig Swistun and not necessarily those of Raymond James Investment Counsel which is a subsidiary of Raymond James Ltd. Statistics and factual data and other information presented are from sources believed to be reliable, but their accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James advisors are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters.

2026 Midyear Market Outlook: Five shifts reshaping markets, On the Horizon, T.Rowe Price, June 2026

Stock market outlook: 3 themes for the second half of 2026, Christopher Buchbinder, Mark Casey, Rob Lovelace, Steve Watson, Capital Group, June 18, 2026

2026 Mid-Year Investment Outlook, Dr. David Kelly and Gabriela Santos, J.P. Morgan, June 17, 2026

TSX ends higher as gold mining shares rally, Fergal Smith, Reuters, June 26, 2026

Global markets weekly update - U.S. inflation rises to highest level since 2023, T. Rowe Price, June 26, 2026

SUBSCRIBE

If you’d like to automatically receive the Weekly Market Update by email, enter your email address in the box below.

We respect your privacy, and you can always remove yourself from the mailing at any time.

Looking to Learn?

If you want to know more about some of the topics we wrote about this week, just click on the links below:

What Are Risk Assets? From Stocks to Cryptocurrencies Simplified