Lexicon Financial Group Weekly Update — April 15, 2026

“An objective financial mindset promotes a careful and balanced approach to investing, avoiding the emotional biases that can disrupt even the best financial plans. It’s a reminder that in finance, as in life, it’s often prudent to step back, assess the situation calmly, and act based on rational analysis rather than getting swept up in the moment’s emotions or trends.”

From the desk of Craig Swistun, CIM, MFA-P, Portfolio Manager, Raymond James Investment Counsel, and Wayne Hendry, Client Relationship Manager, Raymond James Investment Counsel

ISSUE 224

Looking Around

Last week, we revisited how global events impact stock markets and shape their performance. We’re seeing this play out in real time, obviously. But, as someone once said, “We’ve seen this movie before.”

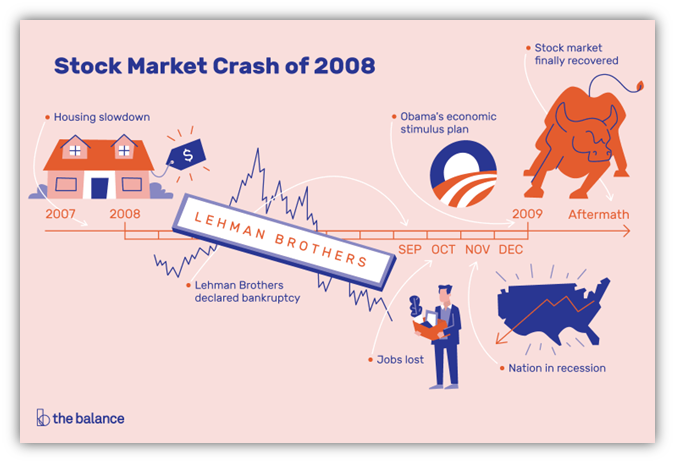

Back in 2008, the U.S. housing market collapsed, triggering a massive financial crisis due to the bursting of an unsustainable, nation-wide bubble that was fueled by subprime mortgage lending and risky financial practices.

Lenders packaged thousands of loans into a single mortgage-backed securities and sold them to investors. When homeowners defaulted, it triggered a collapse in these securities that led to global bank failures and the worst economic downturn since the Great Depression of the 1930s.

Books were written and movies were made. The Big Short (2015) provides a window into the mindset and mechanisms that led to the stock market crash or Great Recession of 2008.

Steve Eisman, an American businessman, investor, and portfolio manager, was at the centre of those discussions. Recently, he has raised concerns about the private credit market.

The private credit market is a market in which non-bank lenders provide debt financing by directly negotiating with a borrower. These borrowers are often small- to mid-sized businesses, and the lenders are usually hedge funds, asset managers or private equity firms. Borrowers make use of private credit as an alternative to traditional bank financing when it isn’t available or is too restrictive for their needs.

Following the financial crisis in 2008, banks tightened lending, so private equity lenders have stepped in to meet demand. Generally, but not always, private credit lenders lend money and pool them into investment packages the same way that the big players did back in 2008. Unlike the purchase of stock in a company, private credit investors are only concerned with receiving interest payments and being repaid their principal. The underlying health of the borrowing company is reduced to a risk calculation – the risk they can’t pay off the loan.

Private credit securities are not publicly traded, and their market is relatively illiquid. The appeal here is that because they bear higher risk, they also have the potential to generate higher returns than a good-old-fashioned-traditional bond. Given historically low interest rates, this market has doubled in recent years. Morgan Stanley estimates that it grew from US$2 trillion in 2020 to US$3 trillion by 2025 and predicts it will continue to grow to US$5 trillion by 2029.

Private credit funds tend to have some mechanisms in place to limit the potential for losses, but generally if a significant percentage of loans in the portfolio default, changes take place. Recently, several large private credit companies have all implemented caps on investor withdrawals. Like Hotel California, you can check out but you can never leave

We don’t invest in private credit for our clients at the moment.

So far, a full-blown crisis has not occurred. There have been no institutional failures like we saw back in 2008 and no spreading contagion within the industry. But that doesn’t mean the problem has been sufficiently contained.

With uncertainty in supply chains, the proliferation of artificial intelligence (AI), and the on-again-off-again tariff situation in the United States (U.S.), it is possible that the next few years will see a wave of corporate bankruptcies as businesses fail to adapt, which could put even more pressure on private lenders who may be forced to put even more caps on the ability for investors to withdraw.

The good news is, according to Phil Bauer, senior vice president and portfolio specialist at Calamos Investments, there is currently little evidence that the recent surge in withdrawals will spiral into a full-blown, systemic crisis. The majority of private credit assets are still predominantly held in locked-up, closed-end vehicles owned by institutional investors – pension funds, endowments, insurers, sovereign wealth funds – who have long time horizons and are much less prone to panic selling. (1)

The bad news is that investors without extremely long time horizons may not be willing to wait for market conditions to improve before accessing their capital. There is nothing worse than not being able to access the cash in your investment portfolio when you need to.

As always, if you have any questions and concerns, please call or email us.

Read and Watch

Want deeper insight into topics in your Weekly Update? Then, read and/or right click:

Should government force Canadian pension funds to invest more in the domestic economy?

Forbes Daily: The Canadian Travel Boycott Is Costing The U.S. Economy

EU’s largest economies vs top US states: How do they compare in GDP?

Japanese PM Takaichi’s Australia visit can shore up energy and economic security

Looking Back

The two-week ceasefire between the U.S., Iran and Israel provided a welcome respite from stock market volatility. The relief rally after this announcement last week was sharp, with equities and bonds moving higher and oil prices down 15 per cent on the news.

Canada’s S&P/TSX composite index rose last Friday and finished up 1.8 per cent last week. This was a five-week high following the news last Friday that domestic data showed subdued jobs growth and investors weighed prospects of a peace deal in the Middle East, with materials, energy and technology sectors among the biggest gainers. On the economic front, Canada's economy added 14,100 jobs in March, which roughly matched expectations after shedding 83,900 in February, leaving the unemployment rate held steady at 6.7 per cent. (2)

Stock markets in the U.S. achieved solid gains (over three per cent) for the second week in a row, as signs of de-escalating conflict in the Middle East and a subsequent drop in oil prices boosted investor sentiment. Enthusiasm around AI-linked stocks also served as a tailwind for parts of the market, with several large-cap technology and semiconductor stocks advancing on optimism around compute demand, new model launches, and continued infrastructure spending. There was some bad news as the Bureau of Labor Statistics reported that its consumer price index (CPI) rose 3.3 per cent year over year in March, accelerating from February’s 2.4 per cent increase. This is the fastest pace since May 2024, although the reading was largely in line with consensus estimates. Almost three quarters of the overall increase was due to a sharp rise in gasoline prices.

The pan-European STOXX Europe 600 Index ended last week up 3.05 per cent in local currency terms, as European markets rallied on news of the U.S. and Iran agreed to a two-week ceasefire.

In Japan, stock markets rebounded strongly during last week, as the worst-case scenario appeared to be avoided, thanks to the U.S. and Iran agreement to a conditional two-week ceasefire. This rebound was driven by technology stocks and other exporters that had been hit hardest by the geopolitical turmoil. Although oil and gas prices plummeted on the ceasefire deal, risks remained heightened amid continued concerns about energy supply disruptions, and the mood was one of caution ahead of upcoming negotiations. Accelerating petroleum prices were reflected in the latest data on producer prices, as the conflict in the Middle East pushed up input costs. Japan’s corporate goods price index (CGPI), a measure of wholesale inflation, rose 2.6 per cent year over year in March. This was ahead of the consensus estimate of 2.3 per cent and following February’s revised 2.1 per cent. Petroleum was the main driver to the headline CGPI, with hydrocarbon chemicals the second-biggest contributor.

China’s stock markets ended the holiday-shortened week higher amid hopes of easing geopolitical tensions following a U.S.-Iran agreement on a conditional two-week ceasefire and expectations for continued negotiations. China’s factory gate prices rose for the first time in more than three years in March, which suggest that the U.S.-Israel conflict with Iran is starting to feed cost pressures into China’s economy.The producer price index (PPI) increased 0.5 per cent from a year earlier, exceeding expectations after 41 months of declines that were driven partly by businesses cutting prices amid intense competition. (3)

The opinions expressed are those of Craig Swistun and not necessarily those of Raymond James Investment Counsel which is a subsidiary of Raymond James Ltd. Statistics and factual data and other information presented are from sources believed to be reliable, but their accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James advisors are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters.

Private Credit 101: What Is It and Why Is There a Redemption Crisis?, Wayne Duggan, US News, March 31, 2026

TSX posts third straight weekly gain as tech and resource shares rally, Utkarsh Hathi and Fergal Smith, Reuters, April 10, 2026

Global markets weekly update - Market sentiment improves amid U.S.-Iran ceasefire agreement, T. Rowe Price, April 10, 2026

SUBSCRIBE

If you’d like to automatically receive the Weekly Market Update by email, enter your email address in the box below.

We respect your privacy, and you can always remove yourself from the mailing at any time.

Looking to Learn?

If you want to know more about some of the topics we wrote about this week, just click on the links below:

Unraveling the 2008 Stock Market Crash: Causes and Aftermath

The Big Short True Story: The Outsiders Who Bet Against America and Won