Lexicon Financial Group Weekly Update — April 8, 2026

“The stock market is a voting machine in the short run, but a weighing machine in the long run.”

From the desk of Craig Swistun, CIM, MFA-P, Portfolio Manager, Raymond James Investment Counsel, and Wayne Hendry, Client Relationship Manager, Raymond James Investment Counsel

ISSUE 223

Looking Around

Before we start talking about this week’s topic, we want to take time to acknowledge Vimy Ridge Day (April 9), and all those Canadians that served.

Vimy Ridge Day commemorates the deaths and casualties of members of the Canadian Corps in the Battle of Vimy Ridge, which took place during the First World War. If you want to learn more about what exactly the Battle of Vimy Ridge was and why it is important for Canadians, please click on the link below to view the recent interview of the Vimy Foundation’s Executive Director Caitlin Bailey by Craig.

https://www.lexiconfinancialgroup.com/gfc_season_two/episode2-vimyfoundation

We need to quickly revisit the impact of global events on stock markets, because they usually play a key role in shaping performance. Stock markets are by nature forward-looking and extremely sensitive to uncertainty. Conflict in Iran sends shockwaves through energy, fertilizer and even the price of helium. Markets scramble to adjust, and investors experience increased volatility in their portfolios.

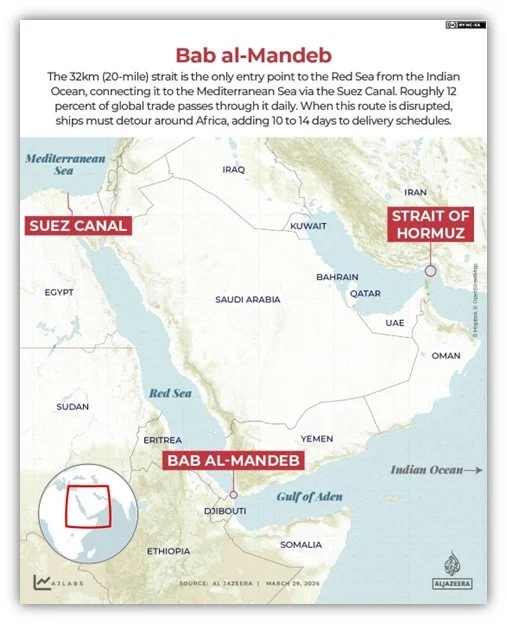

This impact could get worse as, this week, a top advisor to Iran’s Supreme Leader Mojtaba Khamenei threatened that Iranian allies could shut the Bab al-Mandeb shipping route as Iran has effectively done with the Strait of Hormuz.

The Bab al-Mandeb, which connects the Red Sea to the Gulf of Aden, is a crucial waterway for global oil trade and is becoming increasingly more important. Its closure could compound the global energy supply crisis sparked by the conflict, deepening the economic turmoil being felt in factories, kitchens, restaurants, and at gas stations around the world. It is effectively controlled by the Iran-backed Houthis, a Yemen-based group that is a central part of Iran’s so-called “Axis of Resistance” – a coalition of groups ideologically or tactically aligned with Iran. If Bab al-Mandeb and the Strait of Hormuz were both closed to shipping traffic, 25 per cent or a quarter of the world’s oil and gas supply would be blocked.

Saudi Arabia has increasingly turned to its Red Sea port of Yanbu to ship crude using its 1,200 km East West Pipeline, running from the Abqaiq oil processing centre close to the Gulf to Yanbu. The East West Pipeline transferred an average of 770,000 barrels per day (bpd) to the Red Sea coast in January and February. But by the end of March, when the Strait of Hormuz was shut, the pipeline was pumping 7 million bpd which is its total capacity. On top of this, 10 per cent of global trade sails through the Bab al-Mandeb, including containers shipped from China, India, and other Asian countries to Europe. (1)

No sugar coating here. The potential for greater impact on global stock markets here is significant, especially as the double-sided ceasefire that was declared on Monday this week (which lowered oil prices and contributed to a significant rebound in the stock markets) is still fragile. Market volatility will continue as a result. However, history shows that stock markets have been resilient during historical events. From Pearl Harbour to the Cuban Missile Crisis, from the 1987 stock market crash to 9/11, and from Brexit to the Russia-Ukraine conflicts, stocks have repeatedly demonstrated resilience.

According to George Smith, Portfolio Strategist for LPL Financial, looking across more than two dozen major geopolitical events since World War II, the S&P 500 has produced an average one-day decline of just -1 per cent. Smith noted that stock markets generally absorb shocks quickly, stabilizing within 18 days on average and returning to pre-event levels in under 39 days. The scale of the initial event rarely predicts the magnitude of the impact on stock markets. Looking at more than 40 major events — from wars to corporate failures, terror attacks to natural disasters, Smith found three universal lessons:

Markets dislike uncertainty but adapt quickly.

The economic backdrop matters more than the event itself.

Shocks rarely alter long-term fundamentals unless conditions are already fragile.

Smith sees the single most key factor determining stock market performance after a shock is whether the economy is already in or near a recession. When a shock occurs during an economic expansion, stock markets are typically flat to modestly positive over the next month, followed by positive returns over the next three, six, and 12 months. But if a shock occurs near a recession, markets tend to fall across all timeframes, and the average 12-month post-shock return near a recession is -11.5 per cent.

Smith is not alone here as Eric Parnell, chief market strategist at Great Valley Advisor Group, reached a similar conclusion in a 2023 report following the surprise Hamas terrorist attack on Israel. He cited the 9/11 terrorist attacks that forced the closure of the U.S. stock markets for four trading days. Stocks fell by more than eight per cent immediately after the stock markets reopened and proceeded to decline by as much as 15 per cent over the next few trading days, he said. By September 21, stocks had bottomed, and less than a month later, they had recovered all their lost value. By early December 2001, stocks were up by more than three per cent from their pre-attack levels. (2)

Major international events are alarming, and the scope of human suffering is often lost in the sea of data a numbers. Financial and economic markets often don’t pay much attention to the human cost of conflict. However, these dramatic events often trigger notable market volatility.

No one knows where the Iran war will go despite the ceasefire, but history does provide some guidance as to how stock markets might move after major events.

If you have any concerns, please do not hesitate to contact us.

Read and Watch

Want deeper insight into topics in your Weekly Update? Then, read and/or right click:

Canadian oil companies expected to ‘benefit disproportionately’ during the war in Iran

Stock markets continue to rise on hopes of end to Iran war; oil prices move lower

Europe stocks rebound strongly as Trump says Iran war will end in weeks

Crude exports to Japan, South Korea & Taiwan fall 50% y-o-y

How will China’s VAT rebate changes affect the battery market?

Looking Back

Last week, stock markets around the world ended the week hoping for a de-escalation of the Iran war. Despite this, most of them advanced last week.

The S&P/TSX composite index (TSX) ended last week up 3.6 per cent – the biggest weekly gain since November – as a hike in oil prices on fading hopes that the Iran war would soon end boosted energy shares. The price of oil settled 11.4 per cent higher at USD 111.54 a barrel in volatile trading, as traders worried about prolonged disruptions to oil supply the day after U.S. President Donald Trump said the United States would continue attacking Iran. Only two of 10 major sectors of the TSX ended lower last week, including materials, which fell 0.5 per cent as the price of gold fell 1.9 per cent, giving back some of its gains in recent days. (3)

In the U.S., stock markets concluded a volatile, headline-driven week mixed. Thanks to a relatively light economic calendar, most investors were largely focused on shifting geopolitical developments, oil price volatility, and continued pressure on large-cap technology stocks. The Nasdaq Composite led U.S. stock markets higher on its way to logging its best week since November 2025, while the S&P 500 Index and Dow Jones Industrial Average advanced 3.36 and 2.96 per cent, respectively. Smaller-cap indexes also posted good gains. After mostly declining on Monday, stock markets rallied sharply on Tuesday and Wednesday as U.S. President Donald Trump suggested a growing willingness to wind down U.S. military involvement in Iran. Market sentiment weakened again after a Wednesday night address from Trump which failed to provide a clear timeline for de-escalation, pushing oil prices higher and weighing on stock markets. However, they largely recovered by the end of the day, which locked in positive returns for the week due to the Good Friday holiday.

U.S. Treasuries also advanced as yields generally ended lower than the previous week, with the yield on the benchmark 10-year U.S. Treasury note declining from 4.44 to around 4.31 per cent by Thursday afternoon. (Bond prices and yields move in opposite directions.) In addition to the ongoing geopolitical headlines, comments from Federal Reserve Chair Jerome Powell that helped ease some recent inflation concerns also appeared to support fixed income markets during the week.

The pan-European STOXX Europe 600 Index ended the week up 3.92 per cent in local currency terms, as sentiment across the European Union (EU) improved on hopes that the conflict in the Middle East may be shorter-lived than originally feared. Market sentiment was largely driven by uncertainty around how and when the conflict in the Middle East is likely to end and what the likely impact on economic growth will be. The Organization for Economic Cooperation and Development (OECD) has lowered its European growth outlook for 2026 to 0.8 per cent for the year, down from 1.2 per cent. The main reason for this was the conflict in the Middle East, which will raise costs and lower demand. The annual rate of inflation in the eurozone rose to 2.5 per cent in March – up from 1.9 per cent in February. This was the highest rate since January 2025 and was driven by energy costs soaring 4.9 per cent.

Japan’s stock markets fell last week, when its hopes of a firm deadline for ending the war in Iran were dashed, with President Trump threatening to escalate attacks on the country over the next two to three weeks. Investors also received no reassurance about progress toward ensuring that shipping through the Strait of Hormuz would return to normal. As Japan’s economy is highly vulnerable to oil price spikes, given its heavy reliance on oil from the Middle East, this weighed further on market sentiment.

Mainland Chinese stock markets ended last week as markets balanced improving domestic activity signals against persistent external risks. On the political front, China joined Pakistan in its proposal of a five-point peace plan aimed at de-escalating the Middle East conflict, calling for an immediate ceasefire, renewed negotiations, and protection of critical shipping routes, especially the Strait of Hormuz. Both countries called for the protection of civilians and critical infrastructure, including energy facilities, power systems, desalination plants, and nuclear installations. They emphasized the importance of the United Nations and multilateral cooperation in advancing a lasting peace framework.

China also began implementing the removal of the value-added tax export rebates on a wide range of products, including solar components, batteries, and industrial materials, effective April 1. This move is aimed at addressing overcapacity and trade tensions, but it also implies higher export costs and potential margin pressure, potentially accelerating consolidation in affected sectors. (4)

The opinions expressed are those of Craig Swistun and not necessarily those of Raymond James Investment Counsel which is a subsidiary of Raymond James Ltd. Statistics and factual data and other information presented are from sources believed to be reliable, but their accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James advisors are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters.

Iran threatens Bab al-Mandeb closure: How would that affect world trade? Priyanka Shankar and Charu Sudan Kasturi, Al Jazeera, April 6, 2026

Shocks happen, markets move: Lessons from history, Rob Lenihan, The Street, March 4, 2026

TSX notches biggest weekly gain since November as oil soars, Fergal Smith, Reuters, April 2, 2026

Global markets weekly update - Middle East tensions and energy market volatility remain in focus across markets, T. Rowe Price, April 2, 2026

SUBSCRIBE

If you’d like to automatically receive the Weekly Market Update by email, enter your email address in the box below.

We respect your privacy, and you can always remove yourself from the mailing at any time.

Looking to Learn?

If you want to know more about some of the topics we wrote about this week, just click on the links below:

How global events are shaping stock market prices: a look at recent volatility

Crude loadings at Saudi's Yanbu port have continued despite pipeline attack, trading sources say