Lexicon Financial Group Weekly Update — April 1, 2026

“Energy is a linchpin of economic prosperity, with energy security, reliability, and affordability key preconditions for sustainable growth.”

From the desk of Craig Swistun, CIM, MFA-P, Portfolio Manager, Raymond James Investment Counsel, and Wayne Hendry, Client Relationship Manager, Raymond James Investment Counsel

ISSUE 222

Looking Around

The Iran war continues and, as of the time of writing, the Strait of Hormuz remains closed to most commercial traffic. Consumers are being impacted, and not just at the pump. As energy costs increase, companies who ship goods are forced to pass along higher costs. If this sounds familiar, it’s because it is. Higher energy prices are inflationary and make living in a modern economy more expensive.

So, it should come as no surprise that the economic impact of the conflict continues to dominate both traditional as well as social media. It’s even pushed the rise of artificial intelligence (AI) – the dominant new story of 2025 that was poised to define equity markets in 2026 – to the back pages. (1)

But AI is here to stay. Businesses and consumers have become used to the convenience, whether to create spreadsheets faster or more effectively plan a vacation. Here in Canada, we have an abundance of hydro-electric power. It’s clean and cheap. So that might explain why we’re still not hearing a lot about the enormous demand for electricity that these AI systems require to operate.

AI model training and deployment occur mainly in data centres. Picture a giant warehouse in an industrial park that houses servers, storage systems, and networking equipment.

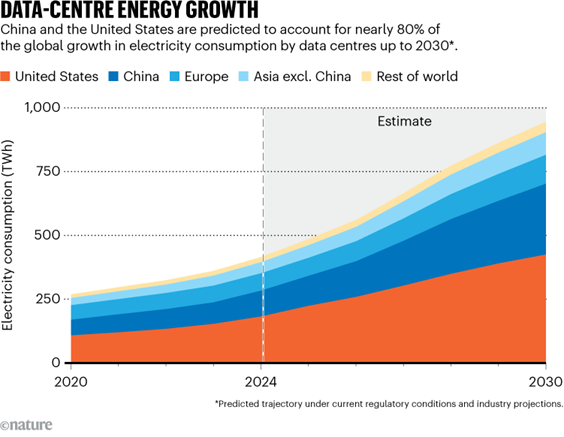

According to the International Energy Agency (IEA), in 2024, electricity consumption by data centres was estimated to amount to around 415 terawatt hours (TWh), or about 1.5 per cent of global electricity consumption. That reflected a 12 per cent per year growth rate over the previous five years. The IEA expects global electricity consumption for data centres to double to around 945 TWh by 2030. The United States (U.S.), China and Europe are projected to be the largest regions for data centre electricity demand over the coming years.

Other regions, however, are experiencing strong growth in data centre development as well. Southeast Asia expects electricity demand from data centres to more than double by 2030. The U.S., though, had the highest per-capita data centre consumption, at around 540 kWh in 2024. This is projected to grow to over 1200 kWh per capita by the end of the decade, which is roughly as much as 10 per cent of the annual electricity consumption of an American household.

And that’s just data centres.

The conflict in Iran has renewed interest in electric vehicles, which only add stress to an already overstressed system in many parts of the world. However, there could be a “changing of the guard” when it comes to power generation and distribution.

Across the U.S. and China, most of the electricity consumed by data centres is produced from fossil fuels (oil, gas, and coal), which is also expected to meet most of the increase to 2030. However, a rising deployment of renewable energies and, later, nuclear power plants is expected to slow the growth of fossil fuel power generation after 2030. In Europe, renewable energies and nuclear power are set to supply most of the additional electricity required by data centres, with their combined share rising to 85 per cent by 2030. Japan and Korea together account for about five per cent of global data centre electricity demand today and by 2030. Renewable and nuclear energy are expected to provide nearly 60 per cent of the electricity consumed by data centres in 2030, up from 35 per cent today.

The rest of the world is responsible for about 10 per cent of total data centre electricity generation, with Southeast Asia and India accounting for a significant portion of that. In both regions, coal is still the main generator of electricity supply to data centres. However, the generation of renewable energy is projected to surpass it by 2035. (2)

The current disruption in oil and gas supplies has injected uncertainty into energy markets, precisely at a time when the world needs more energy. We’re not seeing gradual price increases; prices are jumping as markets attempt to calculate geopolitical risk in real time. The resulting economic impact has made it clear that oil and gas remain a vital part of the global economy, despite the growth and progress of renewable energy technology. (3)

Yet this might be the global wake-up call needed to renew a global push away from fossil-fuel energy sources to renewable energy.

Read and Watch

Want deeper insight into topics in your Weekly Update? Then, read and/or right click:

Xanadu has strong debut as first Canadian tech company to go public since 2021 begins trading

Video - Is US economy, GDP strong enough to offset oil price shocks?

‘Beyond what we could imagine’: Europe’s coming energy crunch

Big Japanese companies are feeling optimistic despite the Iran war — but it might not last

China’s ‘teapot’ oil refineries keep economy brewing – but surging crude prices leave them strained

Looking Back

The Iran war is now into its second month, and its global economic impact continues to grow. Stock markets across the world are illustrating this through increased volatility.

The S&P/TSX composite index (TSX) finished in positive territory (up 2.1 per cent for the week) last Friday, amid losses on U.S. markets, as U.S. President Donald Trump’s extension of a self-imposed deadline to “obliterate” Iran’s power plants if it doesn’t fully allow oil tankers to exit the Persian Gulf through the Strait of Hormuz by April 6 failed to spur optimism.

According to Lesley Marks, Chief Investment Officer of equities at Mackenzie Investments, the stock markets appear to no longer take Trump’s word at face value in the information that he provided about the war. Previously, this information had given people comfort that this would not be a prolonged war and that higher oil prices was temporary. Now, there is greater concern that it will take longer for the U.S. to achieve its objectives, which means greater uncertainty around whether the current oil price environment will persist for a longer period of time. Separately, quantum computing firm Xanadu Quantum Technologies made its debut on the TSX Friday. Its shares gained roughly 11 per cent to close at $16.03. (4)

In the U.S., stock markets concluded a volatile, headline-driven week mixed. A relatively light economic calendar left investors largely focused on shifting geopolitical developments, oil price volatility, and continued pressure on large-cap technology stocks. Although equities rallied to start the week, amid optimism that the conflict in the Middle East could de-escalate, investor sentiment deteriorated through the end of the week, as conflicting headlines appeared to undermine confidence for a near-term resolution. Ultimately, the S&P MidCap 400 and Russell 2000 indexes closed the week higher, both snapping four-week losing streaks, while the S&P 500 Index, Dow Jones Industrial Average, and Nasdaq Composite all finished lower for the fifth week in a row. Large-cap value stocks outperformed their growth counterparts for the third consecutive week.

A preliminary report from S&P Global indicated that U.S. business activity growth moderated in March, with the Flash Composite Purchasing Managers’ Index (PMI) dropping to an 11-month low of 51.4 and down from 51.9 in February. This was largely due to weaker services activity, while manufacturing output strengthened modestly.

The report also highlighted a notable pickup in inflationary pressures, with input costs rising at the fastest pace in 10 months and firms passing through higher prices at the quickest rate since 2022. Businesses widely attributed the increase to higher energy costs and supply disruptions linked to the conflict in the Middle East. Employment also declined slightly, marking the first fall in over a year, as businesses reduced overhead costs in the face of an uncertain economic climate.

The University of Michigan reported last week that its March Index of Consumer Sentiment declined to 53.3, down from February’s reading of 56.6. The report noted that consumers’ short-term economic outlook dropped 14 per cent, while expectations for personal finances in the year ahead declined 10 per cent. Expectations for inflation in the year ahead rose to 3.8 per cent, a 0.4 percentage point increase from February and the largest month-over-month rise since April 2025.

The pan-European STOXX Europe 600 Index rose 0.35 per cent in local currency terms, while other major European markets ended last week mixed. Market sentiment was largely driven by uncertainty around how and when the conflict in the Middle East is likely to end and what the likely impact on economic growth will be. The Organization for Economic Cooperation and Development (OECD) has lowered its European growth outlook for 2026, citing the conflict in the Middle East, which will raise costs and lower demand. It is now forecasting eurozone growth of 0.8 per cent for the year, down from 1.2 per cent. It also lowered its 2026 growth forecast for the UK from 1.2 per cent to 0.7 per cent.

Japan’s stock market returns ended last week mixed. Japan relies heavily on imported energy, and this has raised concerns about higher costs for businesses, slower economic growth, and a potential squeeze on consumer spending. The Japanese government began releasing more state-held oil reserves last week in order to mitigate higher oil prices.

On the economic front, Japan’s nationwide core consumer price index rose 1.6 per cent year over year in February, which was lower than the consensus forecast of 1.7 per cent. The slowdown was largely attributable to government energy relief measures, including subsidies for electricity and gas. The Bank of Japan has indicated that inflation may temporarily soften due to these measures but upward pressure on prices is likely to persist due to surging oil prices.

Chinese equity markets fell last week, as oil price concerns tied to the Middle East conflict surpassed worries about domestic macro issues. China’s government intervened to limit domestic refined fuel price increases and soften the impact of higher energy costs. The National Development and Reform Commission announced that prices for domestic gasoline and diesel would rise by approximately 10 per cent, about half of the increase expected under the government’s pricing mechanism. China is a net importer of oil, and about 45 per cent of its shipments travel through the Strait of Hormuz. On the tariff front, China’s Ministry of Commerce launched investigations into U.S. supply chain and renewable energy practices last Friday. This mirrors the U.S. use of Section 301 tools and marking a further escalation in bilateral trade tensions. (5)

The opinions expressed are those of Craig Swistun and not necessarily those of Raymond James Investment Counsel which is a subsidiary of Raymond James Ltd. Statistics and factual data and other information presented are from sources believed to be reliable, but their accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James advisors are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters.

Outlook 2026 – The Age of Alpha, Fidelity International, November 17, 2025

Energy and AI, IEA-International Energy Agency, April 2025

The Iran war has set in motion a global realignment, Ratko M. Knezevic, Atlantic Council, March 30, 2026

S&P/TSX composite finishes in positive territory, U.S. markets slide as oil rises, The Canadian Press, March 27, 2026

Global markets weekly update - Middle East conflict, energy price volatility drive sentiment across markets, T. Rowe Price, March 27, 2026

SUBSCRIBE

If you’d like to automatically receive the Weekly Market Update by email, enter your email address in the box below.

We respect your privacy, and you can always remove yourself from the mailing at any time.

Looking to Learn?

If you want to know more about some of the topics we wrote about this week, just click on the links below:

How A.I. Companies Are Turning Into Energy Companies

All the Ways the Iran War Is Draining Your Wallet

AI: Five charts that put data-centre energy use – and emissions – into context