Lexicon Financial Group Weekly Update — May 27, 2026

“Interest rates are to asset prices what gravity is to the apple. They power everything in the economic universe”

From the desk of Craig Swistun, CIM, MFA-P, Portfolio Manager, Raymond James Investment Counsel, and Wayne Hendry, Client Relationship Manager, Raymond James Investment Counsel

ISSUE 230

Looking Around

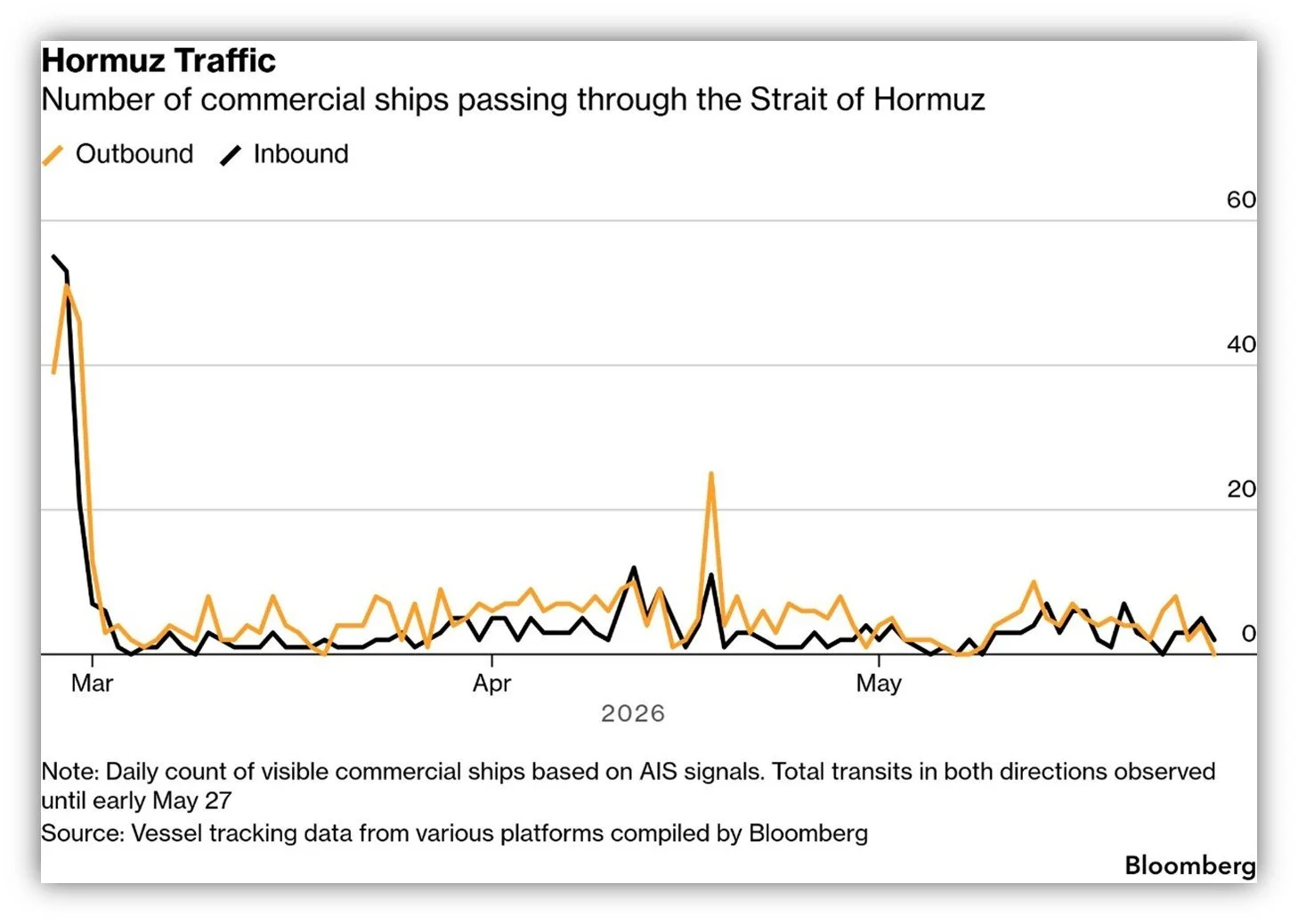

Geopolitical events have an impact on domestic economies. There’s no doubt about that. Inflation has been rising lately, caused by the spillover impacts of the closing of the Strait of Hormuz. Shipping containers, which are vital for the movement of goods and services, have been sitting still on ships for almost two months.

According to the International Energy Agency (IEA), an average of 20 million barrels per day (mb/d) of crude oil and oil products were shipped through the Strait in 2025. This is about 25 per cent of the world’s seaborne oil trade, most of it destined for Asia. This is not to mention exports of liquefied natural gas (19 per cent of global trade), fertilizer or petrochemical production by products like helium.

There are alternative export routes for oil, but they are limited. Saudi Arabia and the UAE have operational crude pipelines that could potentially re-route flows, with an estimated 3.5 to 5.5 mb/d of available capacity, but that won’t clear the backlog. And, when it comes to liquefied natural gas… well, shipping by sea is the only option.

The sheer volume of oil and gas that is exported through the Strait of Hormuz, and the limited options to bypass it, mean that the current disruption to flows will continue to have sizeable consequences for world energy markets. (1)

Consequently, as energy and gas prices rise (or stay higher for longer), central banks will continue to scratch their head about how to control inflation. One traditional method to curb inflation is to raise interest rates. However, that’s where the problem lies. Inflation is growing while economic growth is slowing and it’s still not clear how long the energy shock set off by the Iran war will last. Ongoing peace negotiations are just that: ongoing. For now, most central banks have decided to hold rates steady. The key words here are “for now.”

Some analysts fear that the current energy shock might lead to higher inflation at exactly the time when economic growth is low. This is often referred to as “stagflation.” The last time the United States (U.S.) dealt with persistent stagflation due to an energy shock was in the 1970s and 1980s, and it took double-digit interest rates and two recessions, engineered by the Fed chair, Paul A. Volcker, to defeat it. Central banks do not want to deal with this scenario and hope that the war ends and that these economic problems fade away. (2)

If central banks are forced to increase interest rates, bond yields (the total annual income you earn from bond coupon payments) will rise and current bond prices will drop because investors will want to buy the bonds that offer a higher yield. As demand drops for the bonds with lower yields, their value will likely drop too. We saw this play out a few years ago, when rapid changes in interest rates led to sharp declines in the price of bonds.

It can be unsettling to see the price of your bonds fall when yields rise. The good news is that long-term investors have weathered storms like this before. However, that requires an adequate timeframe to allow some bonds to mature and to reinvest at the higher rates. (3)

Short-term investors may be challenged, but the politicians and central banks certainly are doing everything they can to ease inflation while supporting economic growth. If you have any questions or concerns about the impact to your investment portfolio, we’re always available.

Read and Watch

Want deeper insight into topics in your Weekly Update? Then, read and/or right click:

Why the Bank of Canada won't rush to cut rates, even if Warsh does

Americans Report Lowest Faith in Economy Since 2022

EU in stagflationary trend, must not risk fiscal crisis, ministers say

Japan core inflation softens to over four year low, weakening case for BOJ rate hike

Developments in China’s economy now have a bigger impact on EU: ECB

Looking Back

The S&P/TSX Composite Index (TSX) moved closer last Friday to the record closing high it posted nearly three months ago, as investors increased their focus on high-flying technology shares and awaited quarterly earnings from Canada’s major banks. This helped the TSX end up 1.9 per cent for the week, with the technology sector rising and the industrial sector up 0.5 per cent, and heavily weighted financials ended 0.3 per cent higher. Among the sectors that lost ground was materials, which includes metal mining shares, which fell 0.6 per cent as the price of gold declined. (4)

Last week was a positive week for major U.S. stock markets, with the Dow Jones Industrial Average advancing to an all-time high and the S&P 500 Index rising for the eighth consecutive week—its longest winning streak since 2023. Small-cap and value stocks outperformed large-cap and growth shares, as sentiment improved as enthusiasm around artificial intelligence (AI) stocks—supported in part by chipmaker NVIDIA’s stronger-than-expected earnings results—helped offset uncertainty surrounding the Middle East conflict. Also, despite headlines around a possible deal between the U.S. and Iran remaining fluid and sometimes conflicting, investors generally appeared to see negotiations as more likely than escalating military action.

In economic news, S&P Global released its May Flash Purchasing Managers’ Index (PMI) data on Thursday, which pointed to modest but uneven growth. The composite output index held steady at 51.7 during the month. The inflation components of the survey appeared to be more concerning for investors, as input costs rose at the fastest pace since late 2022, while selling price inflation reached its highest level since August 2022, which reinforced concerns around persistent inflation pressures. The report also noted that employment fell overall, with job losses largely attributed to concerns around rising costs and worsening demand conditions. The University of Michigan’s Index of Consumer Sentiment declined for the third consecutive month in May, dropping five points to a record low of 44.8, with cost-of-living pressures cited as a primary concern.

The pan-European STOXX Europe 600 Index ended last week up 3.00 per cent in local currency terms. Most European markets followed suit and moved higher, driven by rising hopes of a de-escalation in the Middle East. On the economic front, the European Commission (EC), the executive body of the European Union (EU), reduced its economic growth forecasts for the eurozone due to the major energy shock from the Iran war and an already volatile geopolitical and trade environment. It expects gross domestic product (GDP) to grow 0.9 per cent in 2026, down from the 1.4 per cent growth registered in 2025 and lower than its previous estimate of 1.2 per cent. The EC updated its 2026 inflation forecast to 3 per cent, up from the 1.9 per cent it had previously expected.

In Japan, stock markets rebounded strongly during the week, as sentiment was buoyed by ongoing hopes for U.S.-Iran peace negotiations, given reports indicating some progress despite unresolved sticking points on uranium enrichment and control over the Strait of Hormuz. Oil prices also stabilized, which helped support risk appetite. Technology and AI-related shares led the advance, as strong earnings within some semiconductor companies revived global enthusiasm for the AI investment theme and lifted Japan's chip-linked equities broadly. The release of April's national consumer price index showed that Japan's core inflation rate slowed to 1.4 per cent year over year, its lowest reading in four years and below the Bank of Japan’s (BoJ) two per cent target for the third consecutive month. This move reflects an easing of energy-driven price pressures and the continued effect of government fuel subsidies, with the reading coming in below the consensus forecast of 1.7 per cent.

Stock markets in China retreated last week, after disappointing April activity data renewed economic growth concerns. China’s April activity data missed consensus expectations and reinforced signs that first-quarter momentum is softening. Industrial output rose 4.1 per cent year over year, slower than the 5.7 per cent growth in March, while retail sales increased just 0.2 per cent year over year, trailing March’s 1.7 per cent rise. This is the weakest growth since late 2022. Fixed asset investment also contracted 1.6 per cent in the January to April period, highlighting continued weakness in property-related activity and increasing market expectations for additional targeted policy support.

The People’s Bank of China kept its benchmark lending rates unchanged in May for the 12th consecutive month. The one-year loan prime rate (LPR) was maintained at 3.00 per cent and the five-year LPR at 3.50 per cent, which matched market expectations. The LPR serves as China’s benchmark lending reference rate for corporate and household borrowing, while the five-year tenor acts as the primary benchmark for mortgage pricing. This decision reinforced expectations that China may continue to rely more on targeted fiscal and sector-specific support measures rather than broad-based monetary easing. (5)

The opinions expressed are those of Craig Swistun and not necessarily those of Raymond James Investment Counsel which is a subsidiary of Raymond James Ltd. Statistics and factual data and other information presented are from sources believed to be reliable, but their accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James advisors are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters.

Strait of Hormuz Factsheet, International Energy Agency, February 2026

The World’s Central Banks Are Wrestling With a Gigantic Problem, Jeff Sommer, The New York Times, May 1, 2026

What are bond yields? How do rising yields affect investors? RBC Global Asset Management

TSX edges toward record closing high as technology shares climb, The Globe and Mail, May 22, 2026

Global markets weekly update - U.S. consumer sentiment falls to record low amid rising inflation worries, T. Rowe Price, May 22, 2026

SUBSCRIBE

If you’d like to automatically receive the Weekly Market Update by email, enter your email address in the box below.

We respect your privacy, and you can always remove yourself from the mailing at any time.

Looking to Learn?

If you want to know more about some of the topics we wrote about this week, just click on the links below:

Graphic: Tracking ship traffic through the Strait of Hormuz

UN lowers forecast for global economic growth in 2026 over Mideast energy crisis

How Government Bond Yields Relate To Mortgage Rates

Stagflation Explained: What We Learned From the 1970s Crisis