Lexicon Financial Group Weekly Update — May 13, 2026

“The relation between stock exchange and economy is like a man walking his dog. The man walks slowly; the dog runs back and forth.”

From the desk of Craig Swistun, CIM, MFA-P, Portfolio Manager, Raymond James Investment Counsel, and Wayne Hendry, Client Relationship Manager, Raymond James Investment Counsel

ISSUE 228

Looking Around

Just because we’ve seen something before doesn’t mean we can accurately predict how things will end. History doesn’t always repeat.

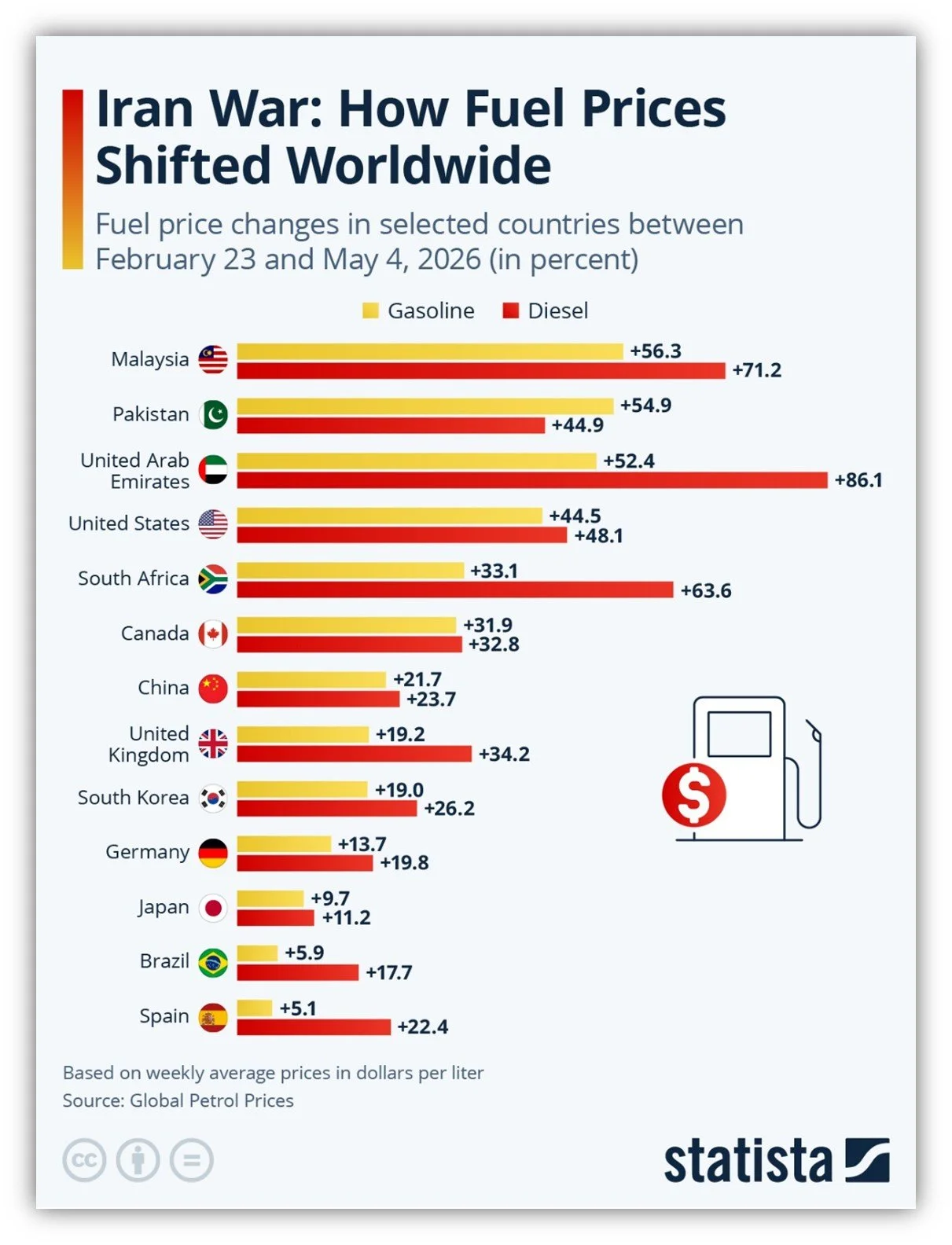

The surge in oil prices that we have experienced since the start of the Iran war proves this point. Historically, sudden oil price surges are a significant drag on stock markets, that frequently cause short-term volatility and contribute to bear markets or recessions by driving inflation up and reducing consumer spending power.

We saw this play out in 2022 (Russia invasion of Ukraine), 1990 (Iraq's invasion of Kuwait), and in 1973, when the Yom Kippur War led Arab members of OPEC to impose an oil embargo against nations supporting Israel. During these and other periods of oil prices spiking 40 per cent or more, stock markets sank.

Brent crude oil, the global benchmark, has traded above US$100 a barrel more than a few times since the outbreak of the current conflict in Iran. This is up 50 per cent and prices have bounced up and down like a ping-pong ball, thanks to the opening and closing of the Strait of Hormuz and a lack of real progress in negotiations. Fuel prices for consumers globally have surged in response.

No one knows when oil prices will begin reverting back to the norm but the economic damage of a continued spike in oil prices is real and continues to grow. A short period of high oil prices on its own isn't enough to cause a bear market or a recession, but the more markets are uncertain, the longer they might take to recover. (1)

Even if peace is achieved and the Strait of Hormuz is open for shipping, the damage to key infrastructure in the Gulf will have to be repaired. According to Rystad Energy, this could be costly and time-consuming to repair, with the total bill potentially exceeding US$50 billion in 2026 and reconstruction of large-scale refining and LNG facilities taking months or even years to complete due to equipment bottlenecks and tight global supply chains for critical components such as turbines and compressors. (2)

Given all of this, we would expect that global stock markets would be more than just volatile. If history repeated, wouldn’t we be seeing more downward pressure on stock markets? Yet, despite being volatile, markets largely recovered their March losses in April and are up for the year.

Why? Even before the start of the war, the U.S. stock markets had proved incredibly resilient to political and economic instability. It took about a year, but they shrugged off the Covid-19 recession and generational high inflation, absorbed Russia’s invasion of Ukraine and increasingly turned a blind eye to Trump’s tariff tiffs. Eswar Prasad, a former IMF official and an economist at Cornell University, argues that investors have a pretty clear view that if there is significant trouble in the financial system, the Federal Reserve (Fed.) and the U.S. government will step in and not let things fall too far. After all, they’ve done that before.

In the U.S., the “K-shaped” economy, which represents the separated experience of Americans whose wealth is tied to the stock market and those who are not, also helps keep its stock markets resilient. Remember that the vast majority of the stock market is owned by just a small percentage of Americans – the top 10 per cent income percentile owns 87.2 per cent of the market, while the bottom 50 per cent own just 1.1 per cent of all stocks. It is the continued spending from the top that has kept many companies afloat as other consumers cut spending. The rising stock market has kept a handful of Americans happy and spending, but there are clouds on the horizon for the current administration, as recent polls show that a majority of Americans currently disapprove of Trump’s handling of the economy, and 63 per cent said they specifically blame him for high gas prices.

That said, tech companies are spending hundreds of billions on artificial intelligence (AI) and the infrastructure needed to support it. This massive investment in AI has been immune to the geopolitical events seen over the last few years and now, just seven companies out of the S&P 500 carry 30 per cent of its weight. They are the usual suspects – Alphabet (Google’s parent company), Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

This enormous spending in AI in such a short space of time has raised concerns among those who believe that there is an AI bubble holding up the stock market. It is worth noting that AI spending outpaced consumer spending as a percentage of U.S. economic growth in the first half of 2025. Historically, this kind of a capital expenditure runs the risk of creating a bubble – remember the dotcoms in the early 2000s? As we all know, there is always a bill to pay for an extravagant meal. (3)

Yet this time might truly be different. Technology companies, by and large, are incredibly diversified.

Take Google, for example (now part of Alphabet Inc.). While its corporate revenues are still dominated by advertising revenue from its search function, it’s highly diversified. It also owns Waymo (self-driving cars), Verily (health care), Calico (longevity), and Wing (drone delivery).

The big lesson that history teaches us is to remain diversified. That’s a lesson worth repeating.

Read and Watch

Want deeper insight into topics in your Weekly Update? Then, read and/or right click:

Canadian Employment (April 2026)

Our economic outlook for the United States - Vanguard

Energy shock drives broader inflation in Belgium - a warning sign for Europe

Looking Back

For last week, the S&P/TSX Composite Index (TSX) ended up 0.6 per cent, as investors cheered the recent growth in corporate earnings, and after weaker-than-expected domestic jobs data in Canada tempered expectations for interest rate hikes. (4)

Stock markets in the U.S. rallied last week due to strong corporate earnings. As of May 7, about 85 per cent of the S&P 500 Index had reported quarterly results. Data from FactSet indicated that slightly less than 85 per cent of these companies announced earnings that topped the consensus estimate. In aggregate, the size of the positive earnings surprise was about 19 per cent. Within the S&P 500 Index, information technology led the way, lifted by encouraging newsflow for companies exposed to AI infrastructure and consumption. However, energy and utilities sectors lost ground.

The pan-European STOXX Europe 600 Index ended a volatile week last Friday with modest gains in local currency terms. Across the European region, sentiment improved early in the week on easing geopolitical tensions in the Middle East and generally strong corporate earnings results. But U.S. President Donald Trump’s threat to put much higher tariffs on the EU if it does not reduce its tariffs on U.S. goods to zero, pressured European markets, and a higher oil price has kept sentiment in check. Other major EU stock markets ended last week mixed. With inflation growing, thanks to the Iran war, the European Central Bank (ECB) is likely to raise interest rates at its next meeting.

Japan’s equity markets were closed Monday through Wednesday last week for the Golden Week holiday. In the shortened trading week, Japanese stock markets ended up significantly higher. These gains were led by a sharp rally in technology and semiconductor shares, supported by continued enthusiasm around AI-related demand and optimism that a potential U.S.-Iran diplomatic breakthrough could ease geopolitical tensions. Falling oil prices helped to alleviate concerns about energy costs and supply disruptions for Japan’s economy, which relies heavily on crude oil imports from the Middle East.

China’s stock markets advanced last week, after reopening following the May 1-5 break, led by technology and select consumer-related shares. Markets were further supported by signs of resilient domestic demand and hopes that Washington and Beijing would focus on maintaining near-term stability in bilateral trade relations. (5)

The opinions expressed are those of Craig Swistun and not necessarily those of Raymond James Investment Counsel which is a subsidiary of Raymond James Ltd. Statistics and factual data and other information presented are from sources believed to be reliable, but their accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James advisors are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters.

Oil Shock: What History Says About the Stock Market and Rising Energy Prices, Jeremy Bowman, The Motley Fool, March 20, 2026

Major Energy Facilities Hit Amid Middle East Conflict, Tristan Gaudiaut, Statista, May 8, 2026

War, inflation and Trump’s tariffs have shaken the US. Why does the stock market keep going up? Lauren Aratani and Andrew Witherspoon, The Guardian, May 14, 2026

TSX notches weekly gain as corporate profits impress investors, Fergal Smith, Reuters, May 8, 2026

Global markets weekly update - U.S. labor market remains resilient, T. Rowe Price, May 8, 2026

SUBSCRIBE

If you’d like to automatically receive the Weekly Market Update by email, enter your email address in the box below.

We respect your privacy, and you can always remove yourself from the mailing at any time.

Looking to Learn?

If you want to know more about some of the topics we wrote about this week, just click on the links below:

Oil Hits $105 But Markets Shrug Off US-Iran Deadlock

The stock market isn’t ignoring Iran. It’s rising for these three very real reasons