Lexicon Financial Group Weekly Update — March 4, 2026

“Those who cannot remember the past are condemned to repeat it. ”

From the desk of Craig Swistun, CIM, MFA-P, Portfolio Manager, Raymond James Investment Counsel, and Wayne Hendry, Client Relationship Manager, Raymond James Investment Counsel

ISSUE 218

Looking Around

Watching the developing conflict in Iran reminds us of Jaws, the four-film series (yes, there were four) – the shark keeps coming back. Last year, conflict broke out in the same region. Fortunately for ordinary people caught in the middle, that conflict was over relatively quickly. At the moment, nobody can reliably predict how long the current war will last. And the shark? It is causing fear and uncertainty in the investing markets, but perhaps not in the way you think.

The war, which began last Saturday, sent jitters through the sectors that make our world run – shipping, fuel, and power. The world runs on energy, and as much as 20 per cent of that crude oil passes through a narrow strait between Iran and United Arab Emirates, called the Strait of Hormuz. Of course, pundits will continue to suggest that we need to reduce our reliance on foreign energy imports. That’s easy to say for a resource-rich country like Canada. Other countries don’t have the same luxury.

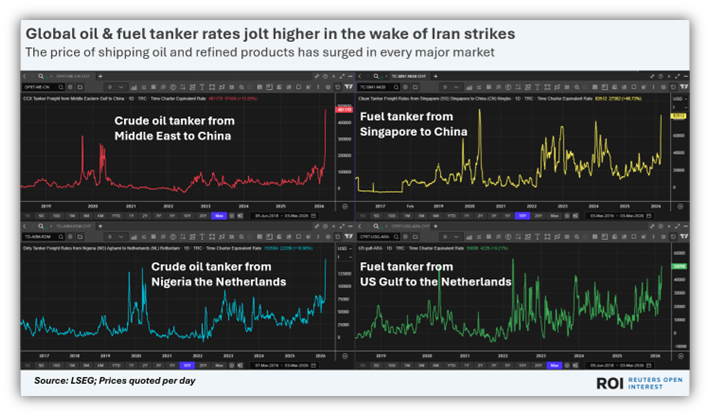

The shipping of oil, fuel and liquefied natural gas (LNG) by the global tanker fleet has been hit hard in the aftermath of last weekend's bombing campaign and the subsequent “closure” of the Strait of Hormuz. Stocks of almost all shipping companies have experienced volatility due to a hit from the traffic disruptions and the subsequent scramble to reroute shipments. Shipping rates for global oil and fuel tankers have jumped in major markets around the world.

For example, quotes for shipping crude oil from the Middle East to China have soared, with the cost of chartering an exceptionally large crude carrier (VLCC) jumping from around US$120,000 a day last week to more than US$450,000. China is the world's largest oil importer and domestic crude oil futures prices have also surged this week, rising by 31 per cent since last Friday compared to 12 per cent increases in Brent and U.S. crude oil futures over the same period.

These price increases will undoubtedly be felt by importers and, where possible, passed along to consumers in the form of higher prices. Energy prices are a key driver of inflation, after all.

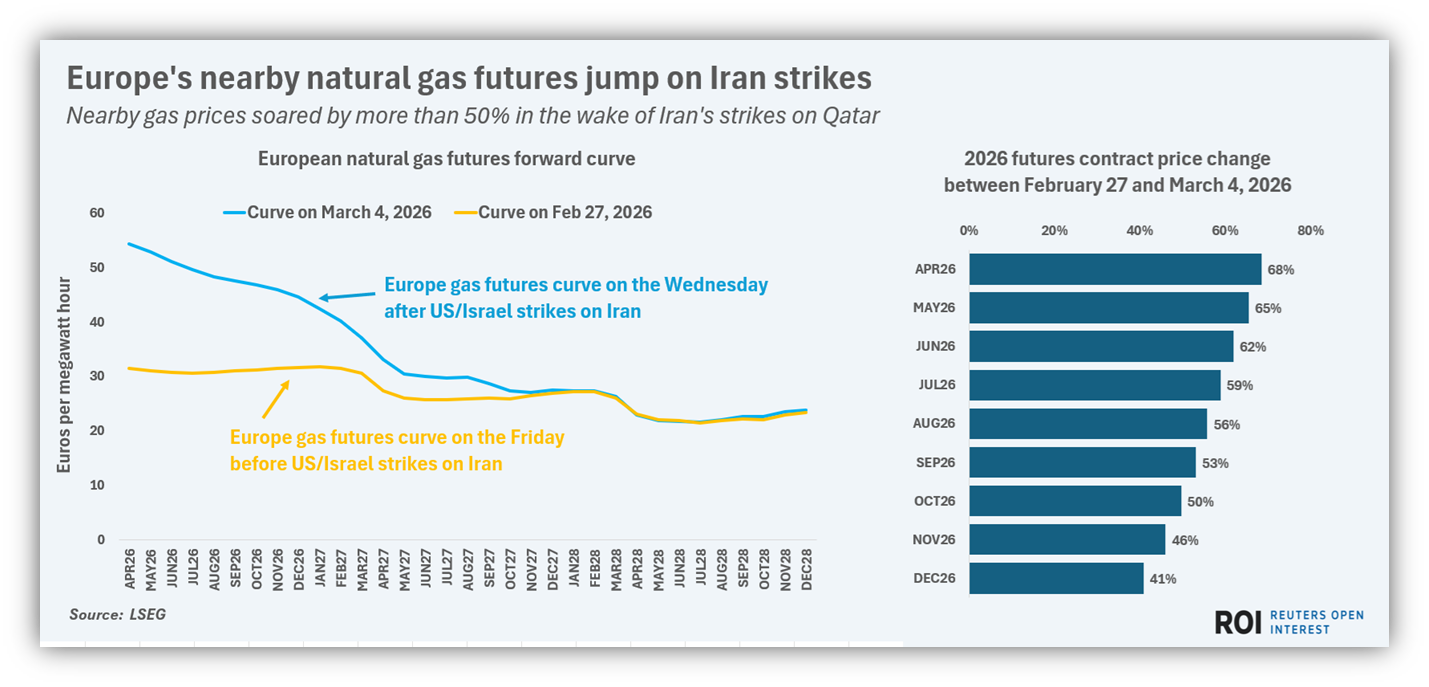

Benchmark European natural gas prices have surged sharply higher, in response to the news that Qatar had paused loadings of liquefied natural gas since its main gas liquefaction facilities were hit by Iranian drones over the weekend. European gas futures contracts have soared by close to 70 per cent since last Friday, while prices for December 2026 have gained around 40 per cent this week on expectations of continuing tightness in global gas supplies.

In the U.S., gasoline contracts have climbed by around 10 per cent since late last week and year-end prices are up by four per cent, as fuel distributors responded to the outlook for tighter global oil supplies and higher shipping costs. This is despite U.S. President Trump announcing steps to restore shipping traffic in the Middle East (including a proposal for the U.S. Navy to escort tankers through the Strait of Hormuz) in order to lower energy costs for U.S. consumers. However, the increasing damage done to energy and logistics channels across the Middle East by the war means that energy prices are likely to continue moving higher, at least for the near term. For now, even higher power, fuel and freight prices could be the norm in the coming weeks. (1)

The current increases are already showing up at gas stations globally. Analysts are saying that a protracted war in the Middle East could see the price of oil reach US$100 a barrel. This would lead to a hike of 20 cents per litre in Canada. In the U.S., the national average for gasoline could reach the US$3-per-gallon mark for the first time this year. This could happen as gasoline demand increases as we move into spring. Higher oil prices will benefit oil producers (Canada included) but spark more inflation, which will make the challenge of affordability for consumers even larger.

Also, let us not forget that the human cost of this war is also growing. According to Bloomberg News, at least 1,200 people have died in Iran so far, and dozens have died elsewhere in the region. (2) These numbers are probably low as it is becoming increasingly difficult to get verified and accurate reporting on conflict at the moment.

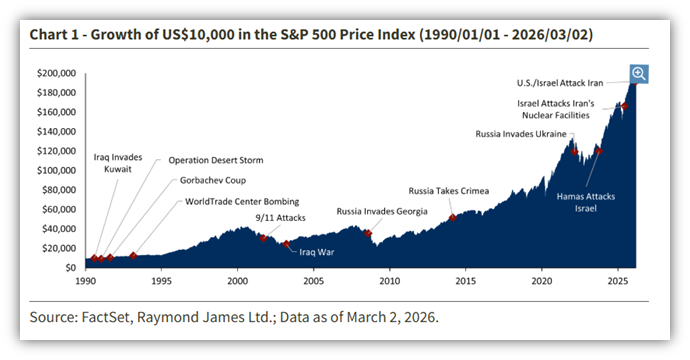

We know for sure that the casualty figure will grow as the war continues. All of this is making investors nervous and stock markets volatile. In the light of this, it is good to remember that we have seen this before. Last year’s war was just the latest in a history of wars in the Middle East and brought with it similar hikes in energy prices, fear in the markets and anxiety globally. And stock markets delivered exceptional performance.

Interestingly, the first three full trading days on the market after war broke out saw markets up. Some will say people had accurately predicted the conflict. Others will say that the cold science of economics does not care. Investment capital continues to move, even while geopolitical games are played out on the real stage and old men shake their fists at clouds. Conflict causes volatility, and while the impact on the ground may take decades to recover, markets tend to smooth these impacts out over extended periods of time.

In the past 35 years alone, we have seen a lot of turmoil. From the Gulf War to 9/11 to Russia invading Ukraine, Gaza and now this. We’ll continue to monitor the impacts in terms of the investment portfolios of our clients and make changes when necessary. That said, we have no plans of abandoning our disciplined approach to investing.

Read and Watch

Want deeper insight into topics in your Weekly Update? Then, read and/or right click:

Canada’s economy has slowed but bank economists point to firmer fundamentals

Iran attacks threaten US economy with more uncertainty around inflation, growth

After Taking a Breather, Why Japan Stocks Could Keep Rising China Economy

China sets its lowest annual growth target on record at 4.5% to 5% as deflation and tariffs bite

Looking Back

Technology and financial stocks weighed on Canada’s main stock index, the S&P/TSX composite index (TSX), as it traded lower last Friday. According to Brian Madden, chief investment officer with First Avenue Investment Counsel, despite this, the TSX still has underlying strength, thanks to gains in the commodities sector as well as defensive stocks like telecom. The TSX finished the week up 1.5 per cent for the week and 8.3 per cent year to date.

Investors, on Friday, also sifted through gross domestic product figures from Statistics Canada (StatCan) for the fourth quarter. GDP, which declined 0.6 per cent on an annualized basis, fell short of expectations from the Bank of Canada and most economists for flat growth. StatCan said the main reason for the contraction was businesses drawing down their inventories — selling off goods or materials that were not reproduced in the quarter. It should be noted that many economists view Canada’s GDP figures as not as bad as the surface number would signify, even though it is really not that good. (3)

Major U.S. stock indexes declined during last week amid ongoing concerns about the disruptive potential of artificial intelligence (AI) and heightened global trade and tariff uncertainty. The Dow Jones Industrial Average led the decline, shedding 1.31 per cent, while the S&P 500 Index lost 0.44 per cent. Stocks started last week on a negative note, selling off on Monday after a widely circulated research report helped amplify worries about potential AI-driven disruption risks to various industries and the broader economy. However, sentiment improved on Tuesday and Wednesday ahead of AI bellwether NVIDIA’s quarterly earnings. Despite this, stock markets ultimately declined through the end of the week, as the chipmaker’s consensus-topping results failed to reverse the broader risk-off sentiment.

On the economic data front, the Bureau of Labor Statistics reported that producer price inflation unexpectedly accelerated in January. The headline producer price index (PPI) increased 0.5 per cent month over month, ahead of estimates for around a 0.3 per cent rise and up from December’s reading of 0.4 per cent. This increase was driven by services prices, which rose 0.8 per cent for the month, the largest increase since July 2025. On an annual basis, PPI inflation came in at 2.9 per cent. This may impact any interest rate cuts by the U.S. Federal Reserve (Fed) this year.

The pan-European STOXX Europe 600 Index hit another new high, as it notched a 0.52 per cent gain in local currency terms last week. Robust corporate earnings and investors’ desire to diversify beyond the technology-heavy U.S. market beat out geopolitical tensions, concerns about AI disruption, and renewed trade tariff uncertainty. Other major European stock markets also ended up last week.

Japan’s stock markets ended last week by achieving record highs to wrap up a strong February, as investors remained optimistic about the policy outlook under Prime Minister Sanae Takaichi. These markets appeared to take in stride the latest tariff announcements from the U.S., with Bank of Japan (BoJ) Governor Kazuo Ueda noting that the 15 per cent global tariff matches existing levies for Japan and is unlikely to have a major impact on Japan. The Tokyo-area core consumer price index (CPI), a leading indicator of nationwide trends, rose 1.8 per cent year over year in February, ahead of estimates of a 1.7 per cent increase and compared with 2 per cent in January.

The recent slowdown in consumer inflation was due largely to renewed electricity and gas subsidies, but the fact that the reading surpassed consensus expectations has lent cautious support to the Bank of Japan’s rate hike trajectory. Separate January data showed that retail sales beat expectations over the month, while industrial production came in weaker than forecast.

Mainland Chinese stock markets rose last week in what was an abbreviated trading week, as risk sentiment improved, and broader market participation returned following the Lunar New Year break and ahead of the upcoming “Two Sessions” meetings. Chinese leaders typically set key economic goals at the annual legislative gathering. (4)

The opinions expressed are those of Craig Swistun and not necessarily those of Raymond James Investment Counsel which is a subsidiary of Raymond James Ltd. Statistics and factual data and other information presented are from sources believed to be reliable, but their accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James advisors are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters.

Charting the widening impact of the Iran crisis on energy markets, Gavin Maguire, Reuters, March 5, 2026

Gas prices: Retailers to pass higher costs on to consumers, says DBRS Morningstar, Jeff Lagerquist, Yahoo Finance, March 5, 2026

Canada, U.S. markets slide on tech weakness as oil prices rise on geopolitical fears, Daniel Johnson, The Canadian Press, February 27, 2026

Global markets weekly update -, U.S. producer price growth accelerates in January, T. Rowe Price, February 27, 2026

SUBSCRIBE

If you’d like to automatically receive the Weekly Market Update by email, enter your email address in the box below.

We respect your privacy, and you can always remove yourself from the mailing at any time.

Looking to Learn?

If you want to know more about some of the topics we wrote about this week, just click on the links below:

Iran Conflict: Seven Takeaways for Investors – Morgan Stanley

From inflation to mortgages, six ways the Iran war could affect your wallet.

Iran war and your portfolio: The historical stock market patterns investors should know