Lexicon Financial Group Weekly Update — June 10, 2026

“Compelling narratives so often beat cold numbers in shaping behavior, markets, and even valuations.”

From the desk of Craig Swistun, CIM, MFA-P, Portfolio Manager, Raymond James Investment Counsel, and Wayne Hendry, Client Relationship Manager, Raymond James Investment Counsel

ISSUE 232

Looking Around

Believe it or not, people still enjoy and respond to stories.

Since the dawn of time, stories have been central to how we make sense of the world. Think of your day: Every conversation, every email, every text, and even your thoughts are made up of short stories or narratives.

From the earliest cave paintings to the latest binge-worthy Netflix series, the art of narrative has always been an integral part of the human experience. (1)

And stories have a way to move stock markets. How? Stories encompass macro-economic factors such as the broader market, economic data, interest rates, geopolitical factors as well as company-specific information such as guidance, earnings, and forecasts. And then there are the stories that analysts, journalists and investors pass around about a company, sector or asset class. This can have a powerful impact on stock prices. With all of the competing narratives, markets today appear to be more narrative- or story-driven than ever before.

A good story can take a complex situation and boil it down to something relatable. We try to do this each week with our updates.

Take Bitcoin, for example. It is down over 20 per cent in the past month, with the most prevalent narrative that investors are selling to free up cash to possibly participate in the SpaceX Initial Public Offering (IPO). Although this may be true, is it provable? Is it a guess? It’s one story. There are others. Making investment decisions based on stories alone is neither prudent nor appropriate. We listen to multiple stories – we share links to some of these stories with readers of the Weekly Update every week – before making any decision.

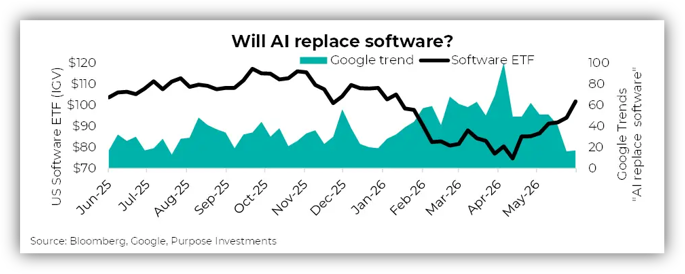

For example, late last year, stories started emerging about the impact artificial intelligence was having on software companies. In a nutshell, if AI can more quickly or cheaply create software, it would pave the way for new competitors to enter the market, selling solutions at lower price points. Valuations of software companies dropped significantly based on the S&P 500 Software index.

This story is no longer headline news. The share prices of the impacted software companies have recouped most of the losses. The story has changed. Stock markets often appear to overreact in the short term and under react in the long term. (2)

The secret here is to listen to stories – both good and bad – but not be swayed by them to the point where fundamental analysis and diversification are pushed aside. And, more importantly for us, it is maintaining the discipline to avoid overreacting, while keeping client portfolios diversified and focused on their unique investment objectives.

Read and Watch

Want deeper insight into topics in your Weekly Update? Then, read and/or right click:

‘Recession is not the word I would use’: Bank of Canada governor

GDP down by 0.2% and employment up by 0.1% in the euro area

Japan wholesale inflation accelerates to fastest in 3 years as energy costs spike

Looking Back

The S&P/TSX Composite Index (TSX) posted its biggest decline in nearly four months last Friday, as commodity prices fell and investors raised bets on Federal Reserve (Fed) interest rate hikes, with technology and metal mining shares leading the move lower. For the week, the TSX was down one per cent. However, Canada's employment report was positive, as Canada’s economy added 87,800 jobs in May, which wiped out much of the declines posted since the start of the year. This enabled the Bank of Canada to hold its key overnight rate at 2.25 per cent. (3)

Unlike the previous week, major U.S. stock indexes finished lower last week. The declines were led by the technology-heavy Nasdaq Composite, which fell 4.68 per cent, followed by the Russell 2000 and S&P 500 indexes, which posted a weekly loss for the first time since March. The Dow Jones Industrial Average held up best by only declining 0.32 per cent.

Early gains tied to AI optimism faded later last week, as investors weighed oil price volatility tied to Middle East headlines, elevated earnings expectations for AI-linked companies, a growing pipeline of AI-related equity issuance, and a stronger-than-expected May payrolls report that helped push Treasury yields higher on Friday. The payrolls report supported the view that the U.S. economy remains resilient but also raised concerns that persistent price pressures could keep the Fed from cutting interest rates this year. Also, initial jobless claims for the week ended May 30 came in at 225,000 – an increase of 13,000 from the prior week and the highest reading since early February. The consulting firm Challenger, Gray & Christmas reported that announced layoffs at U.S. employers increased for the third consecutive month in May, rising 16 per cent from April to about 97,000. The leading reason for this, according to companies, was AI.

U.S. Treasuries generated losses for the week, with yields moving higher across most maturities as solid economic data, oil price volatility, and some hawkish commentary from Fed officials fueled concerns that inflation pressures could keep monetary policy restrictive. (Bond prices and yields move in opposite directions.) After ending the prior week at 4.44 per cent, the yield on the benchmark 10-year U.S. Treasury note increased to around 4.55 per cent last Friday.

Unsurprisingly, the pan-European STOXX Europe 600 Index also declined 0.53 per cent last week. European markets, which also fell last week, seemed to lack direction as investors digested the likelihood of successful negotiations between the U.S. and Iran, a possible ceasefire between Israel and Lebanon, and an announcement on Wednesday by the Trump administration that it is planning on imposing new tariffs of 10-12.5 per cent on many countries. It did not help that, according to final data from Eurostat, the euro area economy shrank by 0.2 per cent in the first quarter—a downward revision from initial estimates that had pegged gross domestic product growth at 0.1 per cent.

Japan's stock market returns were mixed last week, as investor sentiment remained cautious amid the fragile ceasefire between the U.S. and Iran, and with elevated energy prices keeping inflation risks and the outlook for interest rates firmly in focus. The yield on the 10-year Japanese government bond was broadly unchanged over the week at 2.6 per cent. Bank of Japan (BoJ) Governor Kazuo Ueda's latest comments were also interpreted as increasing the likelihood of a June rate hike, as they suggested that responding to inflation should take priority.

Mainland China stock markets ended lower last week, as investors weighed signs of uneven economic recovery amid continued resilience in parts of the private and technology sectors. China's official manufacturing PMI slid to 50.0 in May from 50.3 in April, which indicates that factory activity lost momentum and remained at the threshold between expansion and contraction. However, this survey contrasted with the private sector RatingDog China General Manufacturing PMI, compiled by S&P Global, which remained in expansion territory at 51.8, highlighting greater resilience among smaller and privately-owned firms. For investors, the mixed readings supported the view that policymakers could continue to rely on targeted measures to support domestic demand rather than broad-based stimulus.

Investors also remained focused on China's AI sector, as companies increasingly shift from model development toward commercial deployment. For example, Chinese media reports indicated that China’s popular AI startup DeepSeek could be exploring a potential fundraising round that could value the company at roughly US$ 52 billion. (4)

The opinions expressed are those of Craig Swistun and not necessarily those of Raymond James Investment Counsel which is a subsidiary of Raymond James Ltd. Statistics and factual data and other information presented are from sources believed to be reliable, but their accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James advisors are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters.

Once Upon a Time: A Brief History of Storytelling, Annie Cosby, Freewrite, March 19, 2024

The Narrative Market: Why Stories Are Moving Stocks More Than Fundamentals, Craig Basinger, Derek Benedet, Brett Gustafson & Spencer Morgan, Purpose Investments, AdvisorAnalyst.Com, June 8, 2026

TSX falls the most in four months as oil and gold prices slide, Fergal Smith, Reuters, June 5, 2026

Global markets weekly update - U.S. hiring shows resilience in May, T. Rowe Price, June 5, 2026

SUBSCRIBE

If you’d like to automatically receive the Weekly Market Update by email, enter your email address in the box below.

We respect your privacy, and you can always remove yourself from the mailing at any time.

Looking to Learn?

If you want to know more about some of the topics we wrote about this week, just click on the links below:

Why humans became storytellers

Why Inspiring Stories Make Us React: The Neuroscience of Narrative