Lexicon Financial Group Weekly Update — July 15, 2026

“Wall Street, in the main, hates uncertainty, which manifests itself in depressed share prices of companies whose prospects lack ‘visibility.’ But where the market can err is in confusing uncertainty with risk.”

From the desk of Craig Swistun, CIM, MFA-P, Portfolio Manager, Raymond James Investment Counsel, and Wayne Hendry, Client Relationship Manager, Raymond James Investment Counsel

ISSUE 237

Looking Around

Currently more than 800 wildfires are burning in Canada. Air quality alerts have been announced in Canada and several states in the United States (U.S.) In fact, some states even issued a "hazardous" warning.

The large cluster of fires affecting northwestern areas of Ontario are responsible for sending thick plumes of smoke and poor air quality from Thunder Bay and Toronto. It makes going outside not just unpleasant, but a challenge. Further north, the fires are forcing residents from local First Nations to evacuate and more than a few have lost their homes. (1)

The smoke from wildfires is more than just an inconvenience. It poses significant health risks. These include respiratory problems including triggering asthma, heart disease complications (particles in wildfire smoke can increase the risk of heart attacks and worsen conditions like arrhythmia and congestive heart failure) and other health issues such as increased stress, fatigue, eye irritation, and allergic reactions. (2)

The longer the smoke from the wildfires hangs around, the greater the health risk becomes. There are things we can do to mitigate the effect of wildfires, but it’s obviously better if the fires hadn’t started.

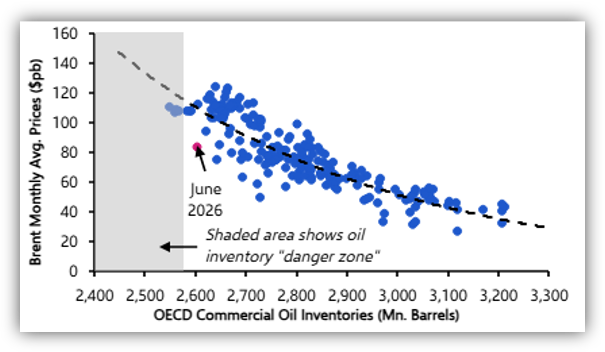

Similarly, undoubtedly the economy and economic projects would be better without a conflict along the Strait of Hormuz (Strait). So far, the global economy has weathered the energy shock, however, a sharp drawdown in oil inventories has left global reserves close to critically low levels.

OECD Commercial Oil Inventories and Brent Crude Prices since 2010

Source: LSEG, Capital Economics

The oil market now has much less capacity to absorb another supply shock. And a protracted closure of the Strait of Hormuz would probably trigger another surge in prices which comes with the risk of higher inflation and a slowing of gross domestic product across the industrialized world. The classic policy response to higher inflation? You guessed it. Increasing interest rates.

The memorandum of understanding (MOU) signed between the US and Iran may have been fragile from the start, but hardliners inside Iran are making negotiations even more delicate. This limits the US ability to declare victory, reopen the Strait of Hormuz and move on. Regardless, markets appear to be still expecting that the disruption to flows caused by the current hostilities will be short-lived and that flows will resume over the coming months, but the perceived probability of a more extreme outcome has increased. However, because the situation is so volatile, a resolution could be reached and prices could fall. It’s really anybody’s guess at this point. We maintain broad diversification in client portfolios to protect against sudden shocks to any single industry sector.

If the Strait does remain effectively closed for longer, we could quickly reach a situation in which oil markets hit a tipping point. A dramatic shock to oil prices has not materialized, in part to about one-third of the crude oil that previously flowed through the Strait being redirected through pipeline infrastructure elsewhere in the region. Additionally, China has sharply reduced its crude imports, which fell by over 40 per cent year-over-year in June as it tapped its vast stock of oil inventories.

Oil inventories cannot continue to be drawn down at their recent pace indefinitely. Higher oil prices would directly impact the global economy where the Gulf economies would be the biggest losers – where recessions would be prolonged – followed by Asia and Europe. China’s export sector has enjoyed an offsetting boom in global demand for green energy products this year, but sharply higher energy prices would undercut this - at US$100 per barrel global consumers might think about buying an electric vehicle rather than a combustion engine vehicle but at US$150 per barrel, they won’t buy a car at all. On top of this, the stagflationary effects of a renewed rise in global energy prices could force central banks to tighten policy and raise interest rates further.

The above scenario is a worst case one which may or may not happen. The best action that investors can take here is to be prepared and not allow fear to drive them to make decisions based on emotion and remain focused on long-term planning. (3)

Read and Watch

Want deeper insight into topics in your Weekly Update? Then, read and/or right click:

Video: Bank of Canada holds key rate steady at 2.25%, predicts economic rebound

Why the US economy stays strong despite Trump’s shockwaves

ECB to hold rates now but energy price resurgence points to September hike: Reuters poll

Our economic outlook for Japan - Vanguard

China's Xi urges global cooperation on AI, warns against single-country dominance

Looking Back

The Toronto Stock Exchange's S&P/TSX Composite index rose to its highest level in more than three weeks on Friday as investors were cheered by Aritzia's earnings report and domestic data showed the economy adding more jobs than expected last month. For the week, the TSX was up 0.1 per cent - its third straight week of gains. (4)

Major U.S. stock indexes closed last week mixed. A late-week rebound in semiconductor and artificial intelligence (AI)-related shares helped the Nasdaq Composite and the S&P 500 Index to rise more than 1 per cent and overcome earlier volatility that was driven in part by higher oil prices and renewed hostilities between the U.S. and Iran. In contrast, the Dow Jones Industrial Average declined, and the small-cap Russell 2000 Index also edged down slightly. Growth stocks solidly outpaced their value counterparts. Within the S&P 500, information technology led sector performance, while the energy and communication services segments also posted strong gains. Materials and health care were the weakest performers.

Trading volumes were relatively light throughout last week due to the limited economic data calendar as well as investors looking ahead to a busy week that includes the start of second-quarter earnings season, inflation data, and the June retail sales report. Minutes from the Federal Reserve’s June meeting showed that a few policymakers saw a case for raising interest rates but ultimately supported leaving borrowing costs unchanged. Officials were somewhat divided over the path for rates through the remainder of the year, given a high level of uncertainty regarding possible economic scenarios, while most supported removing language from the central bank’s policy statement that had implied an easing bias. U.S. Treasuries generated negative returns as rising oil prices and the somewhat hawkish Fed minutes helped push yields higher.

The pan-European STOXX Europe 600 Index ended last week down 1.79 per cent in local currency terms. Geopolitical tensions stemming from the collapse of the ceasefire between the U.S. and Iran collapsed and the two countries exchanged strikes even though they continued to negotiate. Investors considered the possible implications for inflation and monetary policy while markets increased their expectations for European Central Bank tightening. Other major stock markets in Europe also ended down last week.

Japan’s stock markets also fell last week as renewed geopolitical tensions in the Middle East and higher oil prices weighed on investor sentiment. Reports toward the end of the week indicating that the U.S. and Iran would continue peace negotiations despite the escalation in hostilities helped improve risk appetite and limited further declines.

In China mainland benchmarks declined despite a sharp but narrow rally in AI, semiconductor, and other companies that benefited from China’s technology self-sufficiency drive. (5)

The opinions expressed are those of Craig Swistun and not necessarily those of Raymond James Investment Counsel which is a subsidiary of Raymond James Ltd. Statistics and factual data and other information presented are from sources believed to be reliable, but their accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James advisors are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters.

Hundreds of Canada wildfires prompt US air quality alerts as smoke spreads south, Chris Fawkes, BBC Weather, Rachel Flynn and Nadine Yousif, Senior Canada reporter, Toronto, BBC, July 16, 2026

How Long Does Wildfire Smoke Stay in the Air?, FilterBuy, May 5, 2026

The implications of a renewed closure of the Strait, Neal Shearing, Capital Economics, July 16, 2026

TSX rises to three-week high, led by consumer-related shares, Fergal Smith, Reuters, July 10, 2026

Global markets weekly update - Middle East tensions and energy market volatility return to focus, T. Rowe Price, July 10, 2026

SUBSCRIBE

If you’d like to automatically receive the Weekly Market Update by email, enter your email address in the box below.

We respect your privacy, and you can always remove yourself from the mailing at any time.

Looking to Learn?

If you want to know more about some of the topics we wrote about this week, just click on the links below:

Health Effects of Smoke Exposure due to Wildland Fires

IEA chief warns Strait of Hormuz crisis threatens global energy security

Why fully reopening the Strait of Hormuz is such a challenge