Lexicon Financial Group Weekly Update — December 17, 2025

“Volatility is the price of admission. The prize inside are superior long-term returns. You have to pay the price to get the returns.”

From the desk of Craig Swistun, CIM, MFA-P, Portfolio Manager, Raymond James Investment Counsel, and Wayne Hendry, Client Relationship Manager, Raymond James Investment Counsel

ISSUE 209

Looking Around

The end is nigh… for the year that is.

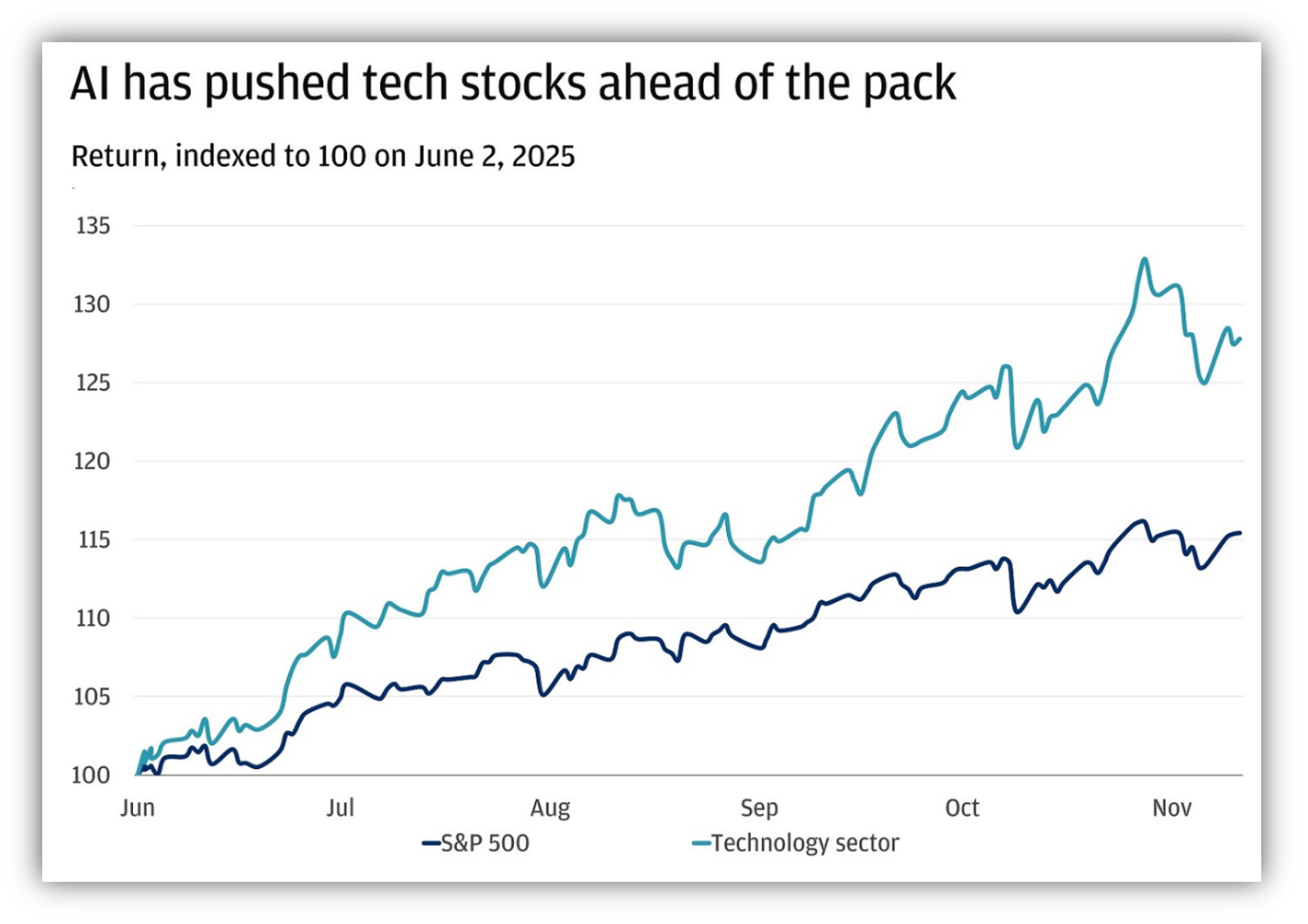

And what a year it has been for investors! Trade wars, the rise of AI, outperformance by the technology sector, tariffs, interest rates… it’s enough to make your head spin. To bring some of this back down to earth, we decided to take a quick look back at some of the key events that shaped the investment landscape in 2025.

Source: Bloomberg Finance L.P. (as of Nov. 12, 2025) and J.P. Morgan Wealth Management

Key moments during 2025 include:

April: Stock markets experienced turbulence due to escalating trade war concerns and tariff policies. Major U.S. stock markets experienced significant drops until an announcement by the Trump administration to pause tariff increases allowed stock markets to rally and stock prices began to recover.

May 13: The S&P 500 index turned positive for the year, signaling a recovery from earlier declines.

June 27: The S&P 500 and the NASDAQ closed at all-time highs, with the technology sector outperforming the broader S&P 500.

November: The U.S. added 64k jobs, but the unemployment rate slightly increased to 4.6 per cent. (1)

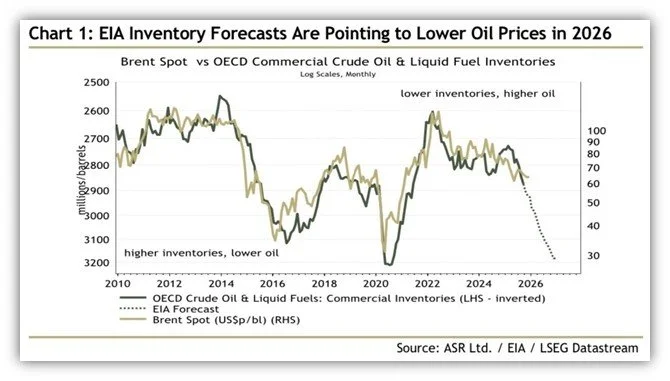

Despite the rise in the overall market in 2025, several sectors struggle, including the energy sector. Geopolitical events influence the price of oil – some can push the oil price down further, while others may push it well beyond current estimates. But, in 2025, oil has been experiencing a pronounced downward trend.

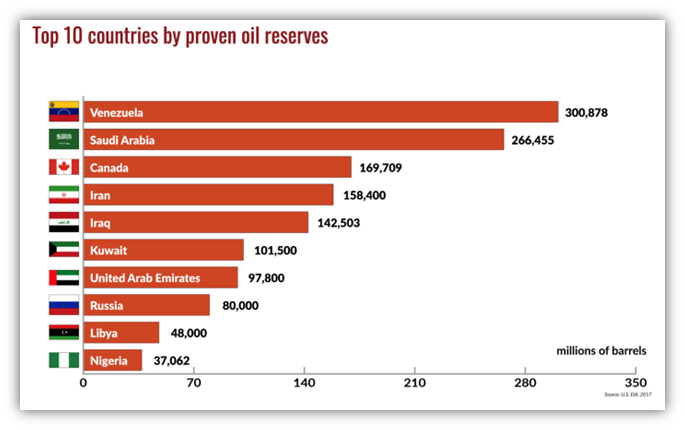

Factors contributing to falling oil prices include current high supply and the pricing in by the markets of a possible reopening of the Venezuelan oil market, if pressure by the United States (U.S.) on Maduro regime in Venezuela increases, and a potential ceasefire between Russia and Ukraine. Venezuela, by the way, has even larger proven oil reserves than Saudi Arabia. (2)

Source: GIS and Market Pulse

Despite challenges in certain sectors, client portfolios have benefitted due to our moderate overweight position in technology. Avid readers of our Weekly Update on January 15, 2025 may recall that we wrote about the positive impact that deregulation, tax cuts, and downward pressure on interest rates in the U.S. would have on the economy.

I know, we spend a lot of time talking about policy south of the border, but for good reason. The United States economy is still the world’s largest by nominal GDP, representing over a 25 per cent of the world’s entire economic output. The sheer size of the market means that, despite volatility, it remains the engine of the global economy.

Another reason we focus heavily on the United States is that it is home to the majority of the world’s largest companies. According to a report by Forbes, 612 of the top 2000 companies in the entire world are headquartered in the United States. By comparison, China is second, with 317 companies listed in the top 2000.

But in the past few years, it has been the mega-cap companies that have been driving economic growth. Sometimes referred to as the Magnificent 7 – Apple, Microsoft, Amazon, Alphabet (Google), Nvidia, Meta (Facebook) and Tesla – these companies have had a massive impact on the global economy. And all of them are listed on the New York Stock Exchange.

What will 2026 bring? We don’t know. One thing we do know is that we wish for each of you a healthy and happy holiday season. We’re also taking a brief holiday break from writing the update but will be back in the New Year, sharing our thoughts with you.

As always, we are here to help or answer any questions you may have.

Read and Watch

Want deeper insight into topics in your Weekly Update? Then, read and/or right click:

Tech stocks weigh on Canadian, U.S. markets while pot stocks surge

Tumbling tech stocks drag Wall Street to its worst day in 3 weeks

AI jitters knock STOXX 600 lower, wiping out early‑week gains

Why Japan's economic woes spark global market concern

China consumer inflation hits near two-year high despite deeper-than-expected producer deflation

Looking Back

Last week, the S&P/TSX Composite Index (TSX) gave back some of its weekly gains on Friday as a drop in technology shares offset sharp gains for cannabis stocks. The technology sector fell 3.4 per cent, with shares of electronics equipment company Celestica Inc. ending 12.9 per cent lower. Heavily weighted financials lost 0.4 per cent and the materials group, which includes metal mining shares, was down 0.7 per cent. The healthcare sector was a standout last week, rising 8.9 per cent while the shares of Curaleaf Holdings Inc. surged 37.8 per cent, after The Washington Post reported U.S. President Donald Trump is expected to push the government to dramatically loosen federal restrictions on marijuana.

For the week, the TSX was up 0.7 per cent as the Federal Reserve (Fed) cut interest rates further and gold prices climbed. (3)

Last week, most major stock indexes rose and hit all-time highs during the week, in the U.S. This was due to the Fed’s third consecutive interest rate cut and commentary from Fed officials that were interpreted by some investors as less hawkish than feared. However, renewed concerns regarding technology stock valuations and questions around whether elevated spending on artificial intelligence (AI) infrastructure will pay off weighed on the tech-heavy Nasdaq Composite, which finished down 1.62 per cent for the week. These concerns were exacerbated after enterprise software company Oracle—which has been a recent beneficiary of AI enthusiasm—announced quarterly revenue results that fell short of consensus estimates on Wednesday, while the company also guided for a substantial increase in capital expenditures.

The Fed concluded its final meeting of 2025 last Wednesday. As was widely expected, it announced that it would lower its target range for the federal funds rate by 25 basis points (0.25 percentage point) to the 3.50–3.75 per cent range. Three policymakers dissented for the first time in six years, with two officials favouring no change to the policy rate and one preferring a 50-basis-point (0.5 percentage point) cut. At his post-meeting press conference, Fed Chair Jerome noted that the Fed funds rate is “within a broad range of estimates of its neutral value” and that policymakers are “well positioned to wait and see how the economy evolves.” He also referenced concerns about “significant downside risks” to the labour market.

Last Thursday, the Labor Department reported that applications for unemployment benefits for the week ending December 6 totaled 236,000 – an increase of 44,000 from the prior week’s revised level. This was the highest weekly total since early September. October’s quits rate fell to the lowest since 2020, which is usually a signal that workers may have less confidence in leaving their jobs and finding employment elsewhere.

The pan-European STOXX Europe 600 Index ended slightly lower, while other major European stock indexes ended last week mixed. Interestingly, the next interest rate move by the European Central Bank (ECB) could be an increase instead of another decrease. A Reuters poll of 96 economists showed that all of them expect the ECB to keep the deposit rate steady next week, while almost 75 per cent expected no change until the end of 2026. This is up from about two-thirds in last month's survey.

In Japan, stock markets rose over last week. The yen (JPY) finished last week broadly unchanged within the JPY 155 against the U.S. dollar range. Markets overwhelmingly priced in the likelihood of a Bank of Japan (BoJ) interest rate hike at its December meeting. This reflects perceptions of improved communication by the central bank, as it seeks to prevent a bout of market turmoil like the one triggered by its July 2024 rate hike, which came as a surprise to many investors.

Stock markets in China retreated as investors took profits after recent months’ gains. China’s November inflation data underscored the weight of deflationary pressures on China’s economy. The consumer price index (CPI) rose to 0.7 per cent in November year on year but the producer price index fell 2.2 per cent, marking the 38th straight month of declines. China has been grappling with deflation since the pandemic ended, amid a prolonged housing slump that has significantly discouraged consumption. The Chinese government has responded by launching a so-called anti-involution campaign aimed at curbing price wars and excessive output in industries ranging from food delivery to car manufacturing. The latest inflation report suggests that its efforts in beating deflation have had limited success. (4)

The opinions expressed are those of Craig Swistun and not necessarily those of Raymond James Investment Counsel which is a subsidiary of Raymond James Ltd. Statistics and factual data and other information presented are from sources believed to be reliable, but their accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James advisors are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters.

2025 stock market crash, Wikipedia, the free encyclopedia, 2025

WTI Oil prices at 2025 Lows – Opportunity or Trap?, Elior Manier, Market Pulse, December 16, 2025

TSX pares weekly gain as technology shares slide, Fergal Smith and Twesha Dikshit, Reuters via MSN, December 12, 2025

Global markets weekly update - Fed lowers interest rates amid rising downside risks to labor market, T. Rowe Price, December 12, 2025

SUBSCRIBE

If you’d like to automatically receive the Weekly Market Update by email, enter your email address in the box below.

We respect your privacy, and you can always remove yourself from the mailing at any time.

Looking to Learn?

If you want to know more about some of the topics we wrote about this week, just click on the links below:

2025 in Review: The Ups, Downs, and Returns of Global Markets

Wall Street Is Shaking Off Fears of an A.I. Bubble. For Now.

Oil prices slip slightly adding to recent losses; oversupply concerns remain